#122: Google 2Q25 = not surprising

Surface-level performance; Deeper metrics; Updated valuation

Don't you dare stare,

You better move.

Don't ever compare

Google to the rest that'll all get sliced and diced,

Competition's payin' the price.

Quo Vadis said knock you out!

Google gonna knock you out!

— LL Cool JThat pretty much sums up Google’s 2Q25 performance. They crushed it. Over the past year, the ad community has spun a lot of Chicken Little rhetoric about the sky falling on Google, particularly around the future of search as we know it. As it turned out, Google is having a Billy Madison moment…

For Quo Vadis, we find it hard to bet against Google’s long track record of superior and consistent returns on invested capital (ROIC) from one period to the next. Our read on 2Q25 indicates things are moving in the right direction for continued growth and outstanding shareholder returns.

We’ve updated our valuation model and price target on the high end of consensus at $280/share. More on that below.

Surface-level performance

Let’s look at surface-level 2Q25 YoY performance and then go deeper into financial metrics to drive the point about what we think is in store for Google shareholders.

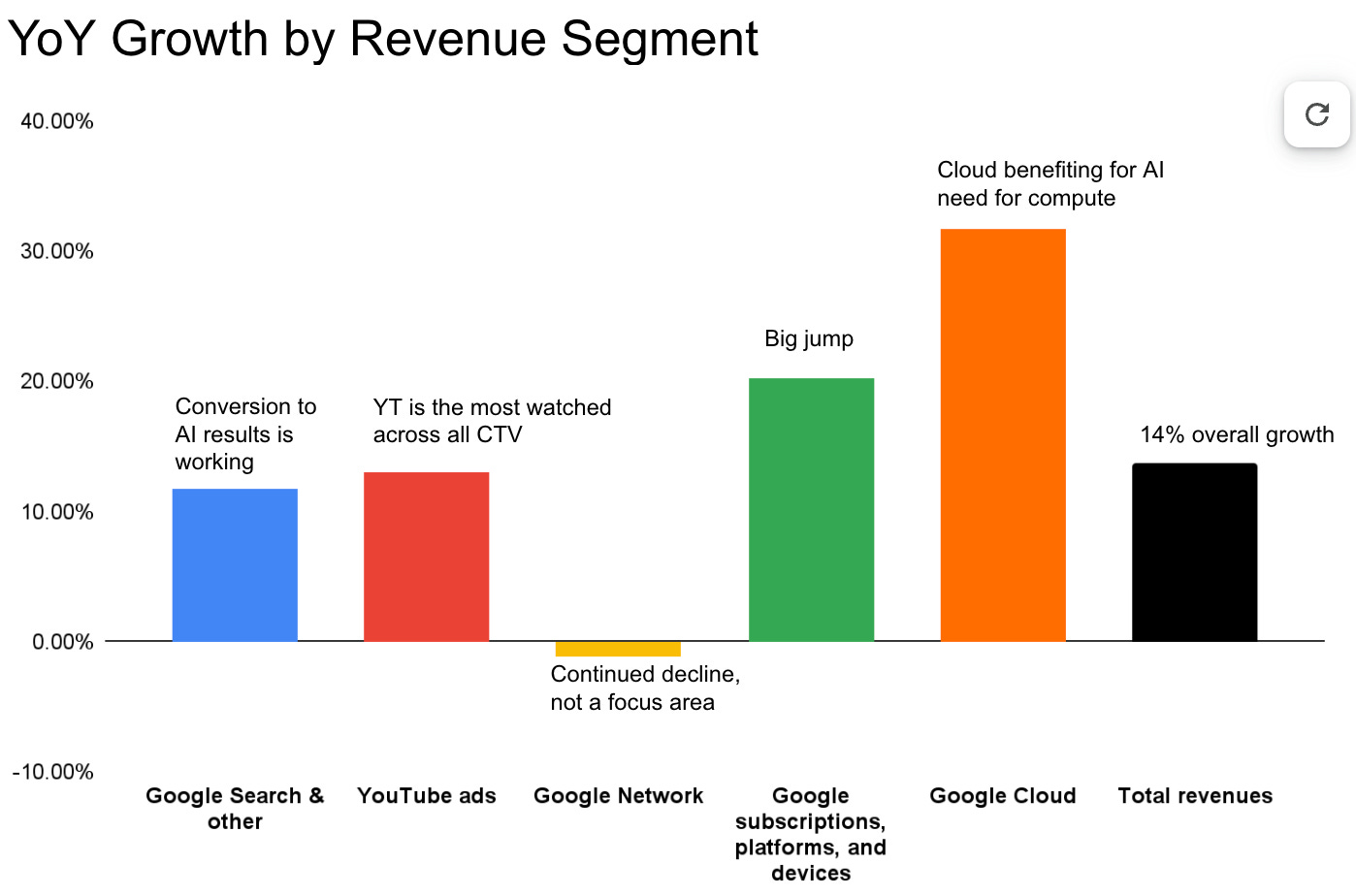

Total revenues up ↑14%. Outstanding for a 26-year-old company.

Google Search up ↑12%. It turns out search is doing just fine as early AI adopters turn into the early majority.

YouTube up ↑14%. The most watched TV streaming service by a country mile and getting better all the time. Nielsen reported that YouTube is in pole position, attracting 12.8% of TV time.

Google subscriptions, platforms, and devices up ↑21%. It’s an $11 billion business with lots of headroom.

Google Cloud up ↑32%. It turns out that all those high-growth ARR AI companies on the Leaderboard, and thousands more, need to procure compute cycles from somewhere. In a market where demand is high and compute supply needs to keep pace with massive investments in new invested capital, there are only a few companies that can play ball. Google is one of them.

Google Network down another ↓-2% and continuing the negative trend that started in 2023.

Question for our readers: Is the decline in Google’s open web revenue performance a leading indicator of things to come for the sector. Is management simply deprioritizing banner ad revenue on websites in slow roll strategy while all hands focus on the bluer oceans of AI?

Search is not dead, it’s just changing (fast)

All in, Google not only printed a great quarter but also put to rest (at least temporarily) the idea that “search is dead.” Search is not dead, it’s just changing. We suspect Google will deliver more solid evidence when it reports Q3 results.

Here’s what Quo Vadis thinks is going on once we distinguish between the job a user wants to get done and how that job gets done. The jobs people do (getting from A to B, heating food, shopping, etc.) are incredibly stable over time. How these jobs get done is what changes.

For instance, observation suggests people use search to get around seven distinct types of jobs done.

Find an answer fast

When I have a specific question, I want to get a reliable answer quickly so I can continue what I was doing. e.g., What time is sunset in NYC? Capital of Mongolia? How to change iPhone wallpaper?

Compare and decide

When I’m choosing between options, I want to compare them easily so I can make a confident decision. e.g., Best running shoes 2025? Samsung vs iPhone reviews? Top MBA programs in Europe?

Explore a topic

When I’m curious about a subject, I want to explore reliable content so I can understand it better. e.g., What is quantum computing? What is the History of the Silk Road? What is AI vs ML?

Solve a problem

When I encounter an obstacle, I want to find a solution that’s been proven to work so I can resolve the issue. e.g., Laptop not turning on. Fix a leaky faucet. Python index out of range.

Plan or execute a task

When I have a task to complete, I want clear instructions or resources so I can get it done efficiently. e.g., Meal prep recipes for young athletes. Build IKEA Kallax. Create an LLC in Delaware.

Feel in control or smart / avoid looking ignorant

When I use search, I want to feel competent and informed so I can trust my decisions. e.g., My boss just said something in a meeting. I have no idea what it is, but I want to look like I do.

Validate or confirm a belief

"When I believe something, I want to find proof that supports it so I feel reassured or justified. e.g., Coffee is good for health. Is Tesla S better than Mercedes E-Class?

These seven jobs have been remarkably stable throughout time. What’s changed is how people get it done. In every innovation cycle, including AI, it comes down to getting a job done better, faster, cheaper. That’s what Google is investing in now to protect and grow the search moat it has built up with $252 billion in total invested capital put into the business since day 1.

We can also look at what’s changing from the perspective of three personas:

“Older people use ChatGPT as a Google replacement. Maybe people in their 20s and 30s use it as like a life advisor, and then, people in college use it as an operating system.” — Sam Altman, May 2025

Persona 1: Google replacement (better answers)

How do I pair my new headphones to an iPhone?

Find five top-rated Italian restaurants near Savannah and give me average dinner prices.

Persona 2: Life advisor (personal decisions)

Help me decide between staying at my tech job or joining a 10-person startup.

Help me make a budget to pay off $15K in student loans in 3 years and still save for a wedding.

Persona 3: Operating system (context-rich and continuous)

Plan my week. Classes are in the attached schedule. I work Tues and Thurs 4–8 pm. Soccer practice Wed 6–8 pm. I need 1.5 hours a day for studying.

Write a Python script that texts me at 6:30 am if it’s going to rain during my commute."

From Google’s perspective, and looking at the $47 billion in new fixed invested capital put into the business since 1H24, it seems more than reasonable to believe management is investing in all three personas at the same time.

Myth: AI is replacing employees

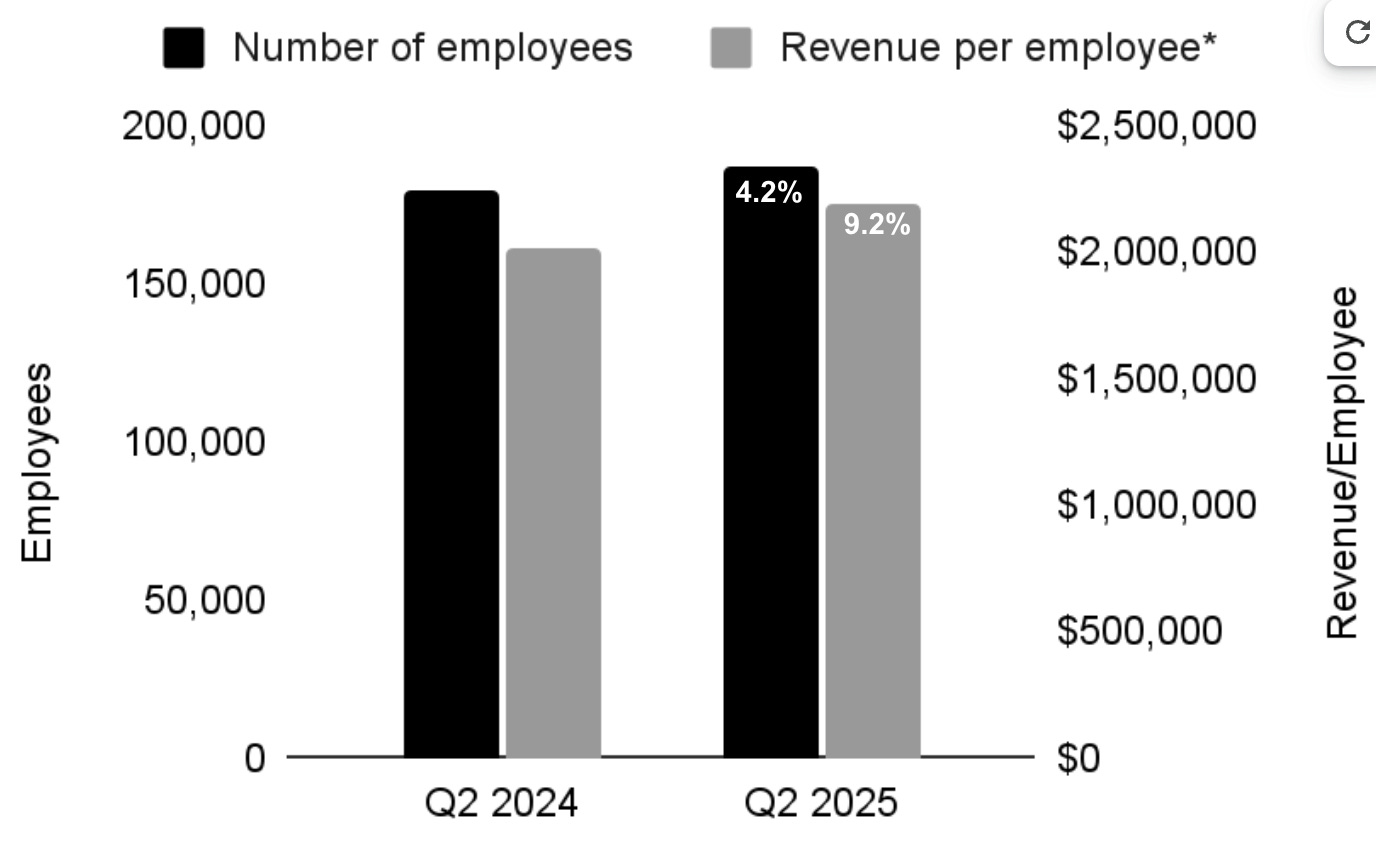

Interestingly, Google reported 179,582 and 187,103 employees from 2Q24 to 2Q25, respectively. While various sectors of the economy are going to require less human labor (e.g., college graduate entry-level jobs) as AI replaces routine tasks and enhances productivity, Google is going in the opposite direction.

Not only did Google grow its employee count from 2Q24 to 2Q25 by 4.2% (7.5K new Googlers), but it also grew revenue per employee disproportionately by 9.2%. Talk about a surprise to the upside! This is certainly something we’ll be keeping an eye on over the coming quarters for Google and other adtech players.

A quick aside about the history of digital automation and global unemployment

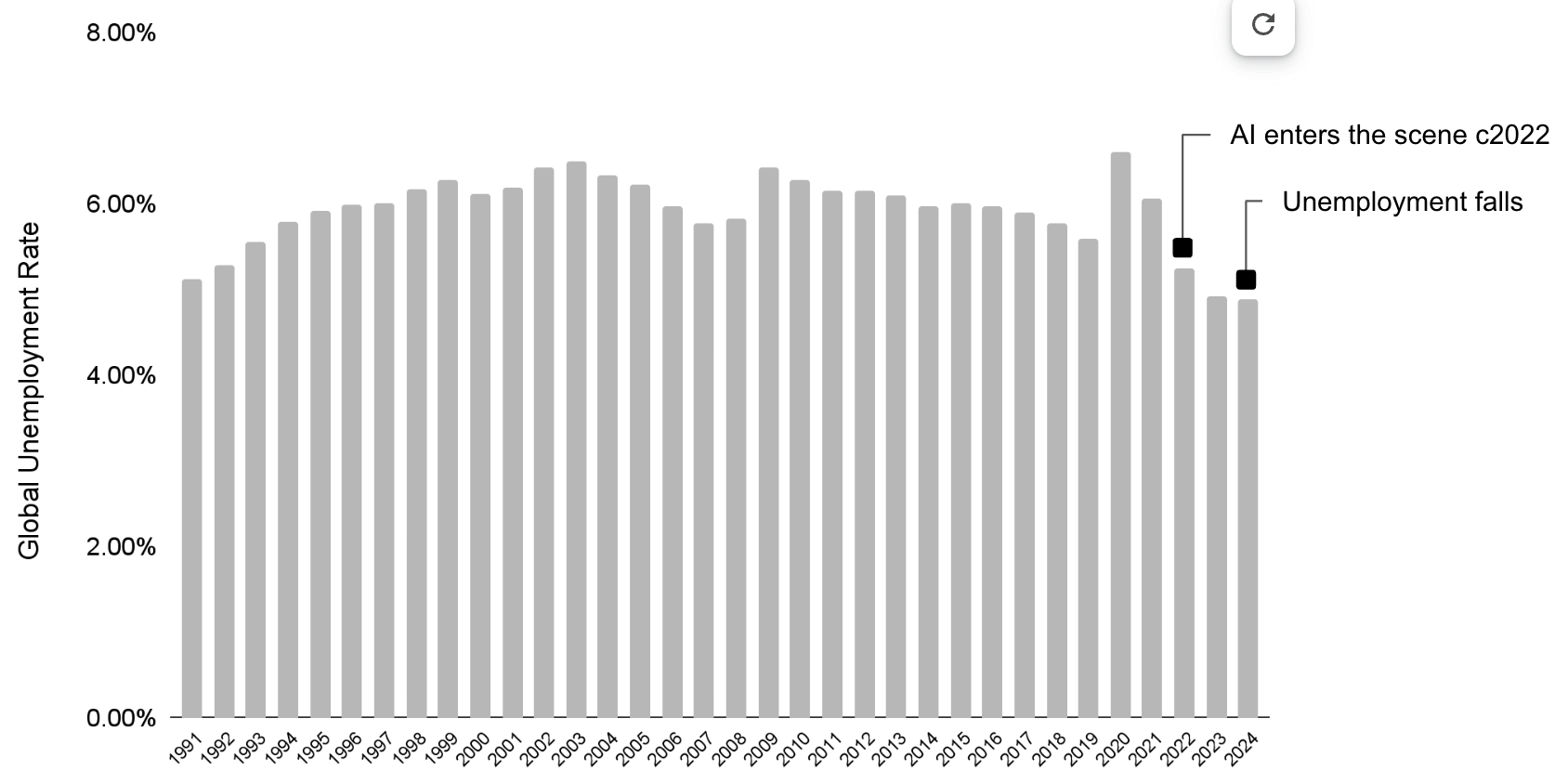

As we look back at the history of every major innovation cycle, it seems the headline-grabbing fears that AI will replace tons of jobs and cause an increase in unemployment are a bit overdone and unsupported by the data.

Look at global unemployment going back to 1991. The average unemployment rate is 5.9% yet the current rate is sitting at 4.9%. Where are all the unemployed people? What happened with the argument “it’s different this time?” Over the past 25 years of the last innovation cycle (Internet/Big Data), the entire world worked its way through massive digital transformation and ended with more employment.

Back in the early 1990s “experts” expressed concern that the internet and digital automation would lead to higher unemployment, yet the exact opposite happened. That kind of technological anxiety wasn't new. Fears about job loss due to automation date back to the Industrial Revolution.

Sure, certain jobs were indeed displaced, but the Internet also created entirely new industries and millions of jobs. Just like other general-purpose technologies from yesteryear, the Internet’s impact on employment was transformational rather than purely subtractive. And there is zero reason to bet against the same thing happening as a result of the current AI innovation cycle.

Going deeper into Google’s performance metrics that matter most to valuation

As our readers know, there are four things we care about most when it comes to valuation:

Revenue growth is about attracting customers and maintaining or increasing prices

Net operating profit margins after adjusting for cash taxes (e.g., the taxes that would have been paid (and will eventually be paid) after disentangling GAAP accounting constraints

Return on Invested Capital (ROIC) is about separating operating assets/liabilities from non-operating assets/liabilities like excess cash, goodwill, and long-term investments.

Fundamental Growth Rate (g), an area Google continues to shine after 26 years.

Revenue growth

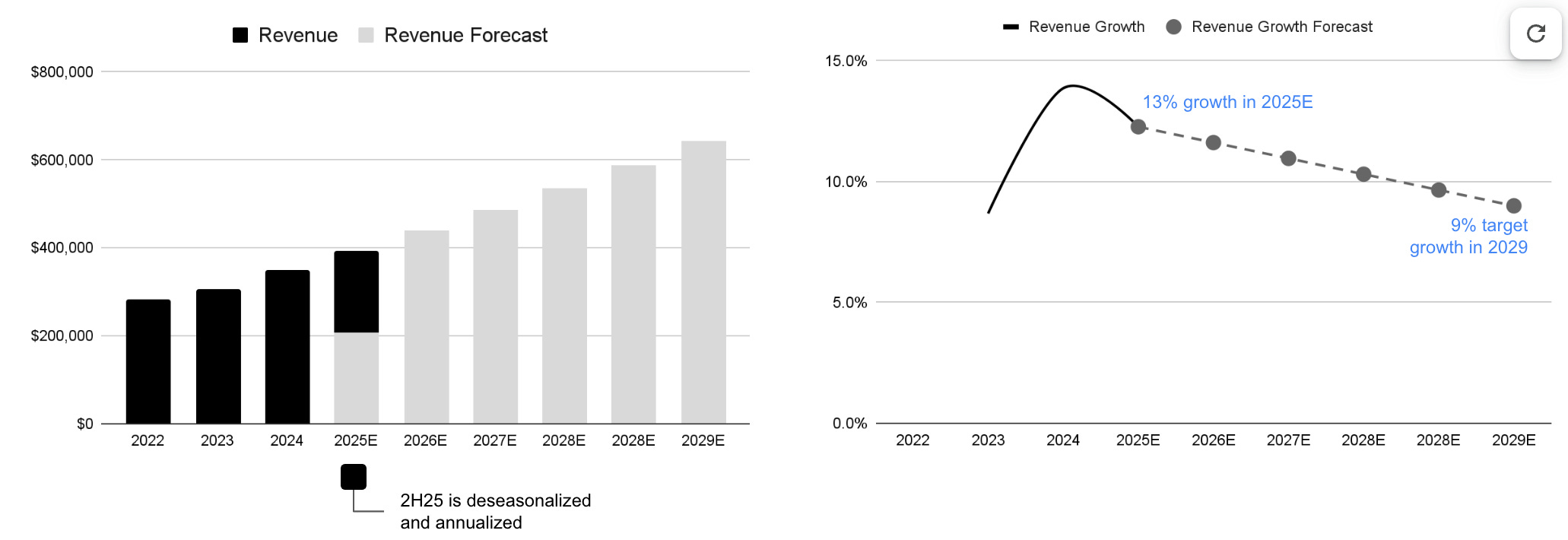

Looking at revenue first, Google’s mousetrap continues to beat a path to many advertisers’ doors. After deseasonalizing and annualizing what Google has delivered in 1H25, we estimate $393 billion for full-year 2025 revenue.

Going forward, we conservatively set 2029 revenue growth at 9% and work backward on a linear trend, resulting in a gradual downward trend line. Even with conservatism on our side, Google’s 2029 revenue grows to ~$640 billion.

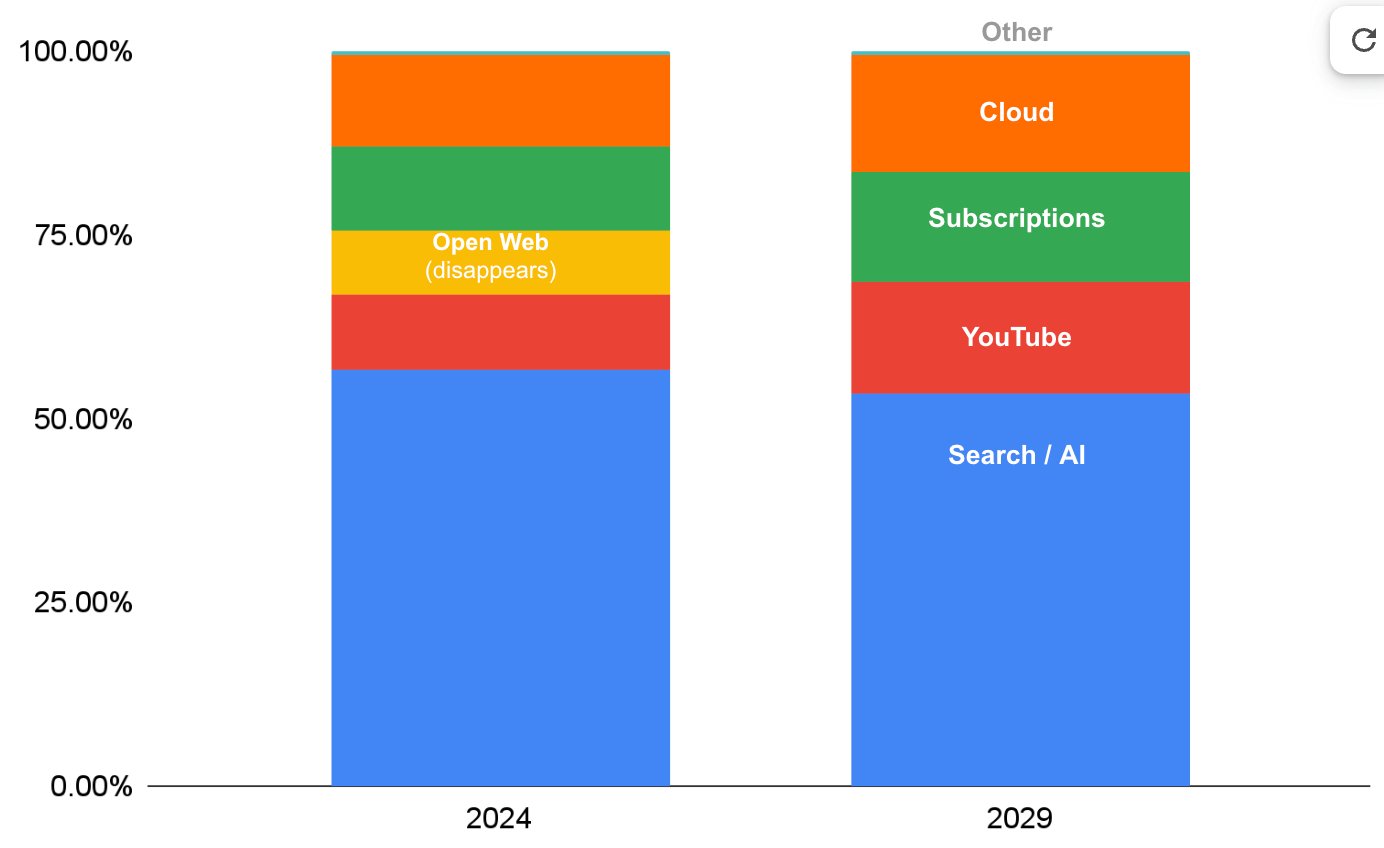

Here’s how we see it playing out by segment:

Google Search continues to decline from 57% of revenue in 2024 to 54% in 2029, implying $340 billion in search revenue on a 12% CAGR (inclusive of AI-related search revenue).

YouTube partially displaces the declining search share, moving from 10% of revenue to ~15% and dominates the CTV world.

Let’s get a bit crazy and say Google Network moves from 9% of revenue today to 0% as Google exits the open web by 2029 (or perhaps sooner). The free cash flow generated from a giant open platform (DSP, SSP, and Ad Server) will help fund AI investments over the coming years.

Google subscriptions, platforms, and devices move from 12% to 15% of revenue.

Google Cloud grows from 12% to 16% of revenue (maybe more) as the demand for AI compute grows.

Other bets and hedging revenue remain more or less constant at ~0.5% of revenue.

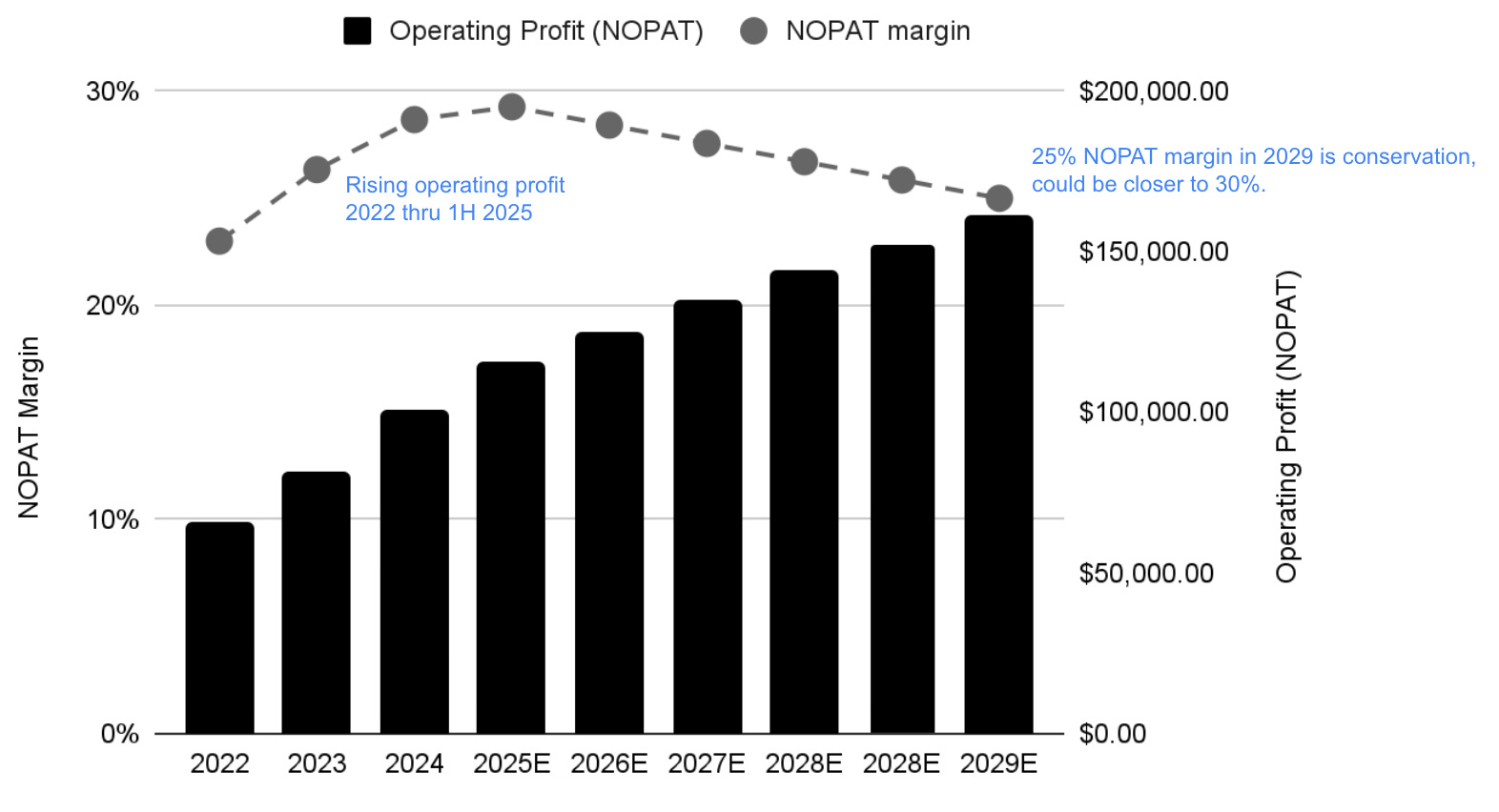

Operating Profit Margin

Before 2023, Google’s average net operating profit margin (NOPAT) was around 22% and improved through 2024 and into 1H25 at 29%. Not many companies get north of 20% let alone approach 30% operating margins.

As we look down the road with a margin of safety in mind, we see zero risk in assuming 25% operating margins in 2029.

Return on Invested Capital (ROIC)

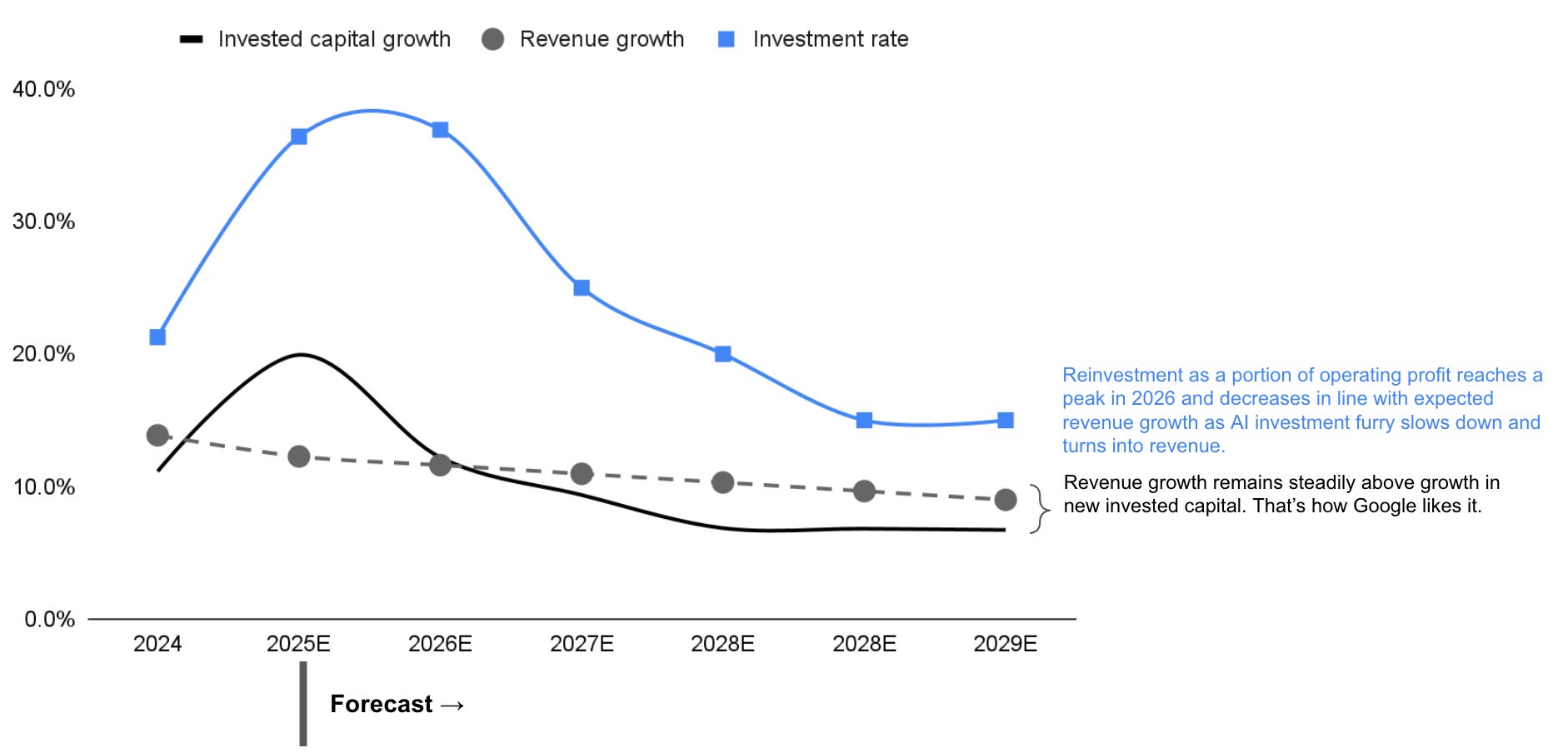

ROIC is simply a function of net operating profits and invested capital. Invested capital breaks down operating working capital plus operating fixed capital (aka capex). From the end of 1H24 to 1H25, Google’s new investment in fixed capital grew by 33% ($47 billion referenced above) as it pushes into all things AI.

As a rule of thumb, over longer periods of time, invested capital growth rates will be lower than revenue growth rates. However, during new innovation cycles like we are seeing with AI, many companies like Google, Meta, Microsoft, and thousands of venture-backed startups are making big bets. For Google, its big AI bet materializes in the bump in the chart above.

When it comes to financial rigor, Google is a bit different than most other companies. Since 2013, Google’s compounded annual revenue growth rate is 18% but its YoY invested capital CAGR is 20%. That’s unusual and very smart for Google’s shareholders. Most other companies grow invested capital at half the rate (or lower) of revenue… and then they wonder why revenue growth is so sluggish.

Reinvestment Rate: Since 2013, Google’s average reinvestment rate (new invested capital as a portion of net operating profits) has been 31%. And from 1H24 to 2H25, it was nearly 37%. As discussed above, that rate of investment is not sustainable or necessary over the long term.

As we try to imagine the next five years, we think Google’s invested capital growth rate will stabilize back toward expected revenue growth rates and remain reasonably above revenue growth.

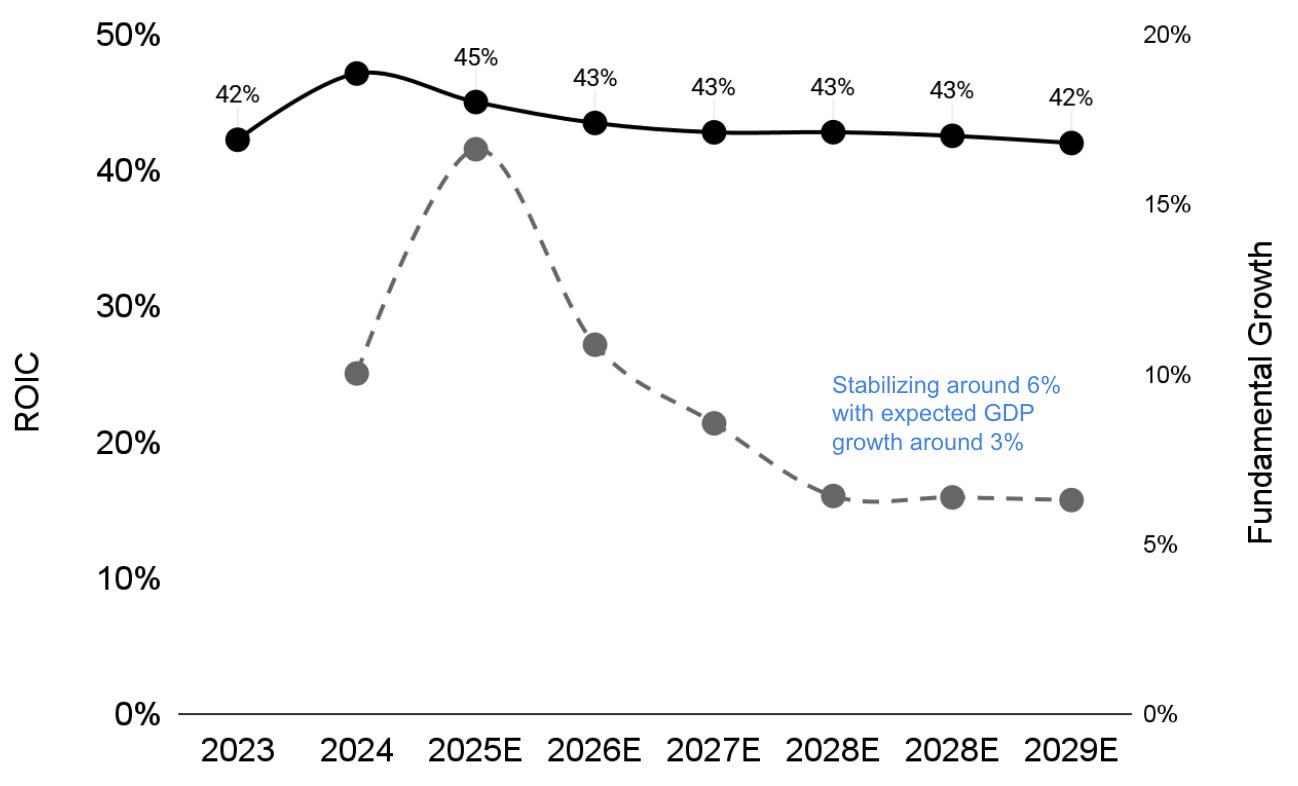

ROIC and Fundamental Growth:

Given the revenue growth rates, net operating profit margins, and investment rate highlighted above, Google will stay on a steady ROIC path well north of 40%. Keep in mind, our 25% NOPAT target margin could be closer to 27% in 2029, and revenue growth could also beat our conservative assumptions.

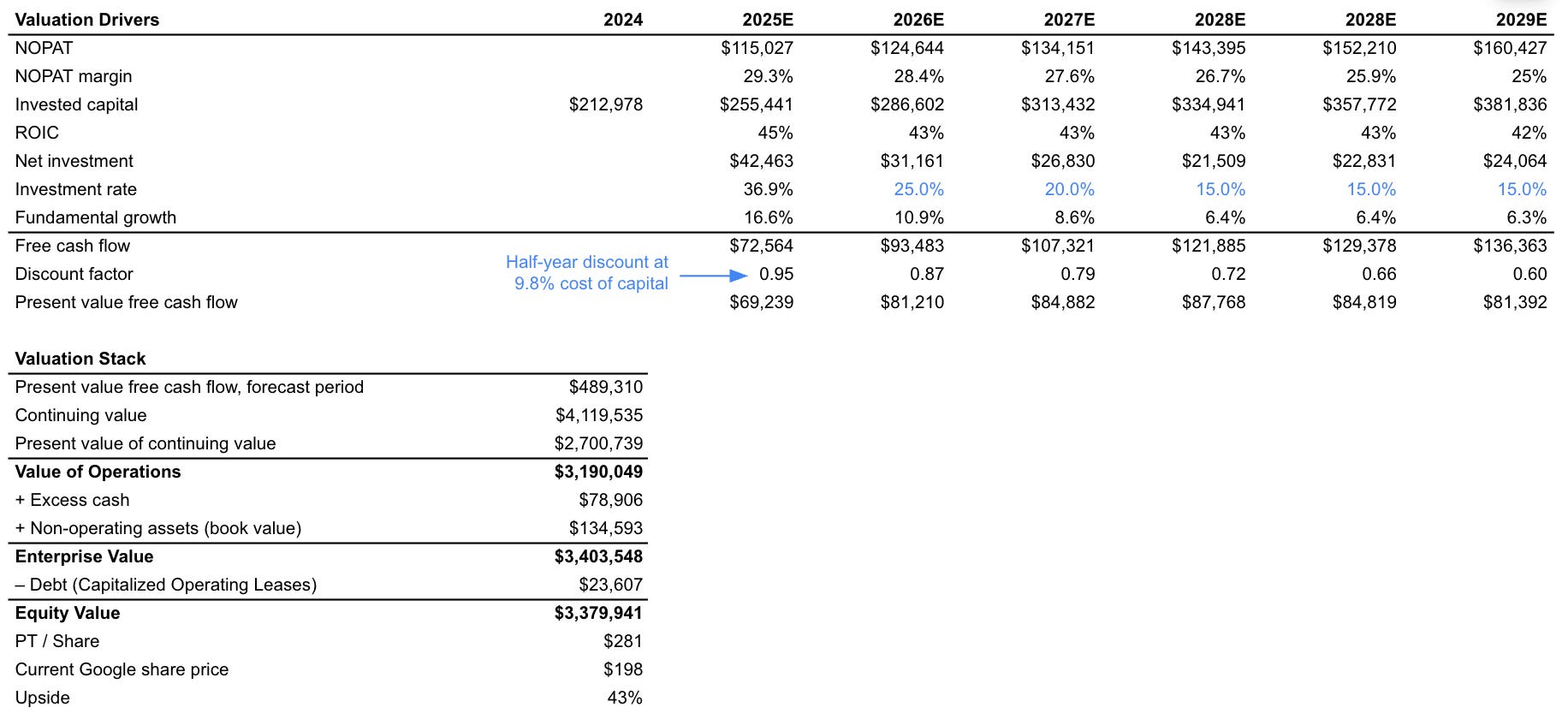

Valuing Google

Here’s how we land on a $280/share price target. Start with $160 billion in net operating profit in 2029.

We take net operating profit margins from 29% today to 25%. Seems like a safe bet.

We taper Google’s investment rate from the recent high investment in AI downward, but still above expected revenue growth.

If that plays out, ROIC might decline a bit, but it remains very healthy over the foreseeable future.

As the older markets mature and get displaced by new markets, fundamental growth for Google (and all companies) will slowly decay toward global GDP growth (e.g., ~3%) in the distant future.

All in, it’s more than reasonable to see Google as an undervalued company as it heads into the next chapter of exceptional returns for investors.

Disclaimer: This post, and any other post from Quo Vadis, should not be considered investment advice. This content is for informational purposes only. You should not construe this information, or any other material from Quo Vadis, as investment, financial, or any other form of advice.