#123: Trade Desk 2Q Earnings

Valuation reset; Implied math behind investor mindset; Sigmoid opportunity

If you're interested in staying ahead of the curve in AdTech and MarTech, then don’t miss the upcoming season of the Landmark Ventures Executive Roundtable Series called DEAL — Dialogue on Exits, Acquisitions & Landscape. This off-the-record event brings together top executives, investors, and founders to discuss the most pressing market shifts and transaction signals through the lens of AI's impact. These “round table” sessions are designed to deliver actionable insights and foster valuable connections. Quo Vadis will be there. Register here.

Trade Desk 2Q earnings, valuation reset

“They gon' try and bring you down, hating's what they do. But you gotta keep a smile, stay up on your move.”

— Mac Miller

The Trade Desk reported 2Q earnings last week on 19% YoY revenue growth. You’d think investors would be okay with that kind of growth, but they sold off shares on the news, taking the stock down nearly 40%.

Although management’s guidance is in line with estimates, investors appear to want more growth. Management guided to $717 million in net revenue for Q3, translating to 14% YoY growth. The trend line likely spooked investors with 25% YoY growth in Q1, 19% in Q2, and now 14% expected in Q3.

Perhaps most alarming for investors were earnings call comments like:

“Amazon is not a competitor, and Google really isn't much of a competitor anymore either.”

There is only so much media money to go around across all the main channels in the following order of priority (more or less): Linear TV, CTV, Social, Search/Retail Media, OOH, and then Open Web Display. When we see Amazon’s ad business growing like mad while Google delivered a massive Q2 (search and YouTube), it’s hard to dismiss those two as formidable competitors looking to expand their bite in the media pie.

As far as open web ads go, TTD is always in the spotlight as the biggest breakout success story, so it was not surprising to see LinkedIn and X light up with social commentary on the Q2 earnings drop. Some of it was good and interesting, but Brian Wieser put it best in Madison and Wall:

“In the case of The Trade Desk, we have a solid #2 ad tech business (with Google the presumptive #1) that hasn’t yet made much progress outside of the US or expanded beyond its core product, but also isn’t going anywhere any time soon. Towards those ends, any disappointment at sub-20% growth rates in the future probably reflects overly optimistic expectations from outsiders rather than poor execution from the company itself.”

The implied math behind a changing investor mindset

Let’s go super deep and take a peek into TTD’s valuation from the perspective of how investors think about valuing companies, either explicitly in a purposeful way or implicitly in a subconscious way.

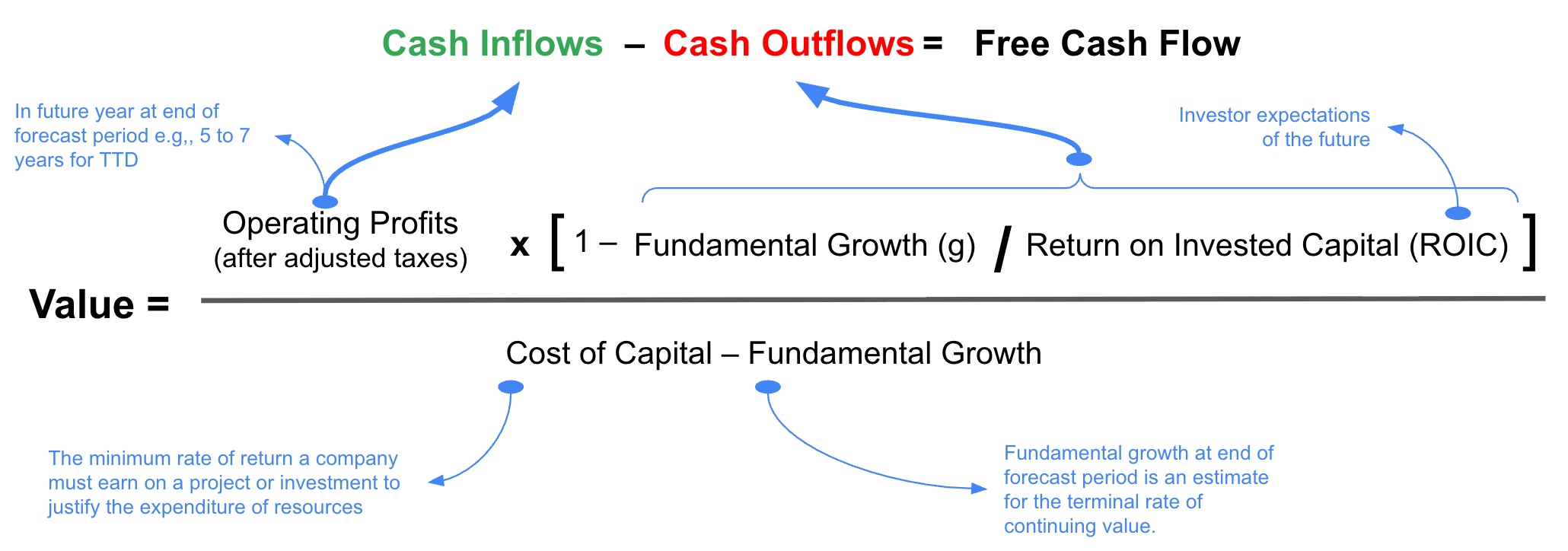

We’ll do this by breaking down what Tim Koller at the McKinsey Finance Institute calls the Zen Formula of Valuation and look at TTD’s Q2 repricing through that lens.

Like everything else in valuation, this is an imperfect exercise, but quite interesting to gain a better understanding of investor psychology. Why? Because over the long run, all the statistical evidence shows that market capitalization and stock market returns are ultimately driven by Return on Invested Capital (ROIC) and fundamental growth (g). That’s the beauty of deep fundamental valuation… you get the best idea of where stock is heading independent of market emotion and sentiment.

Over the short run, investor sentiment, enthusiasm, and various cognitive biases can cause a disconnect between what investors think something is worth compared to what it is really worth when past assumptions get updated with new information and new thinking.

Here’s what this little formula says:

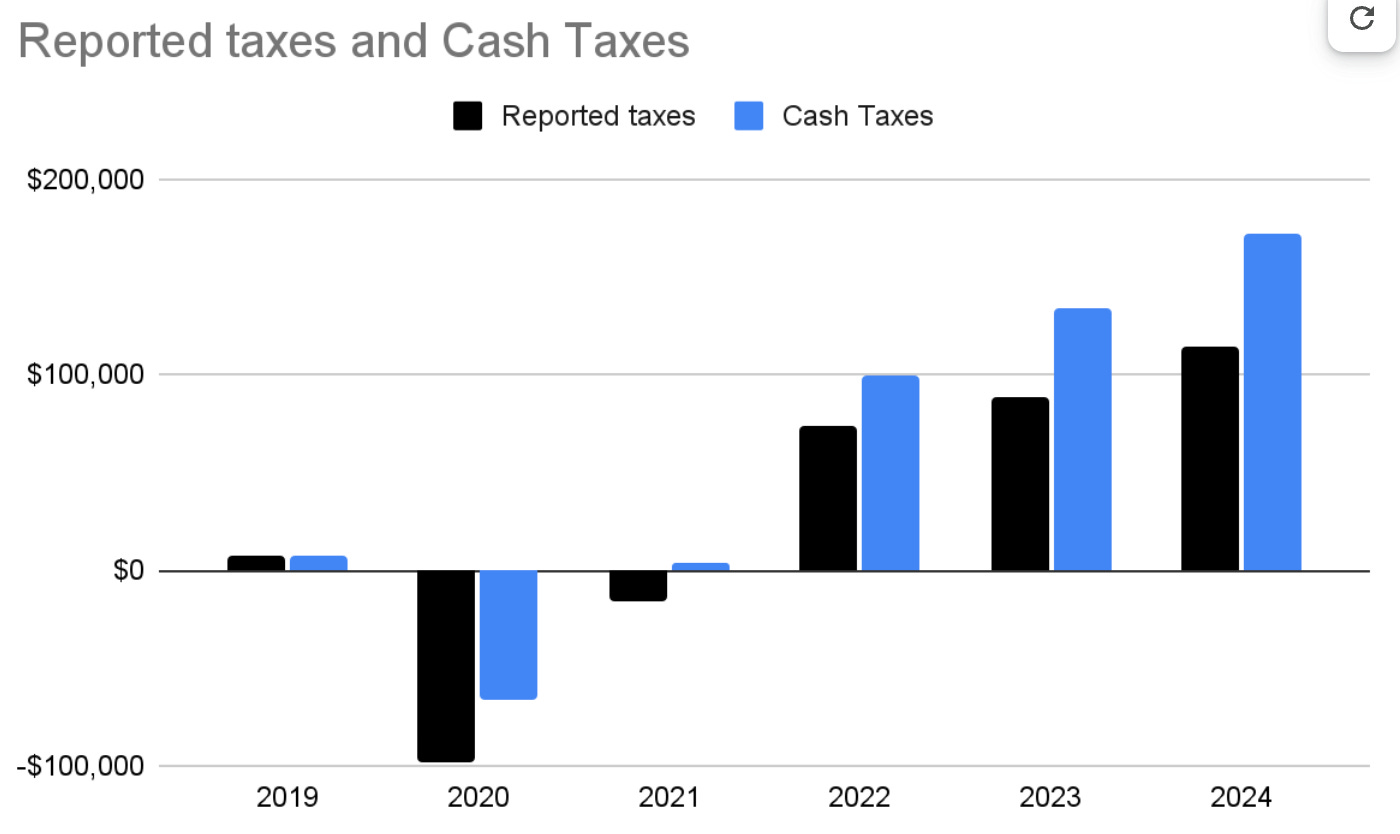

Operating profits after adjusting for actual cash taxes, as opposed to the accountant’s tax calculations on the income statement (see chart below). From the investor’s perspective, they are thinking (explicitly or implicitly) about what operating profits (cash inflows) will be in the foreseeable future (e.g., a 5 to 7-year forecast for TTD is sufficient).

The second term bracketed in the numerator is a mathematical shortcut for a company’s investment rate, which is simply the change in working capital and capex as a portion of operating profits. For instance, if a company increases invested capital from $100 to $110, and operating profits are $40, then the company invested $10 back into the business, which is 25% of operating profits. That’s the investment rate. Said another way, if a company is growing operating profits (aka fundamental growth) at 6% with a 35% ROIC, then its investment rate is 17% (6% ÷ 17%).

The numerator as a whole is free cash flow. Investors want management to maximize cash inflows while making smart investment choices to keep growing the business in the future, which are cash outflows. The difference is free cash flow. Investors always want free cash flow maximization. When companies deliver, they get rewarded with a higher stock price. When investors get nervous about the level and certainty of future cash flow, they tend to bail out.

The denominator simply accounts for both the risk (cost of capital) and the potential for future growth (g), which together shape how much a company's future profits are worth today.

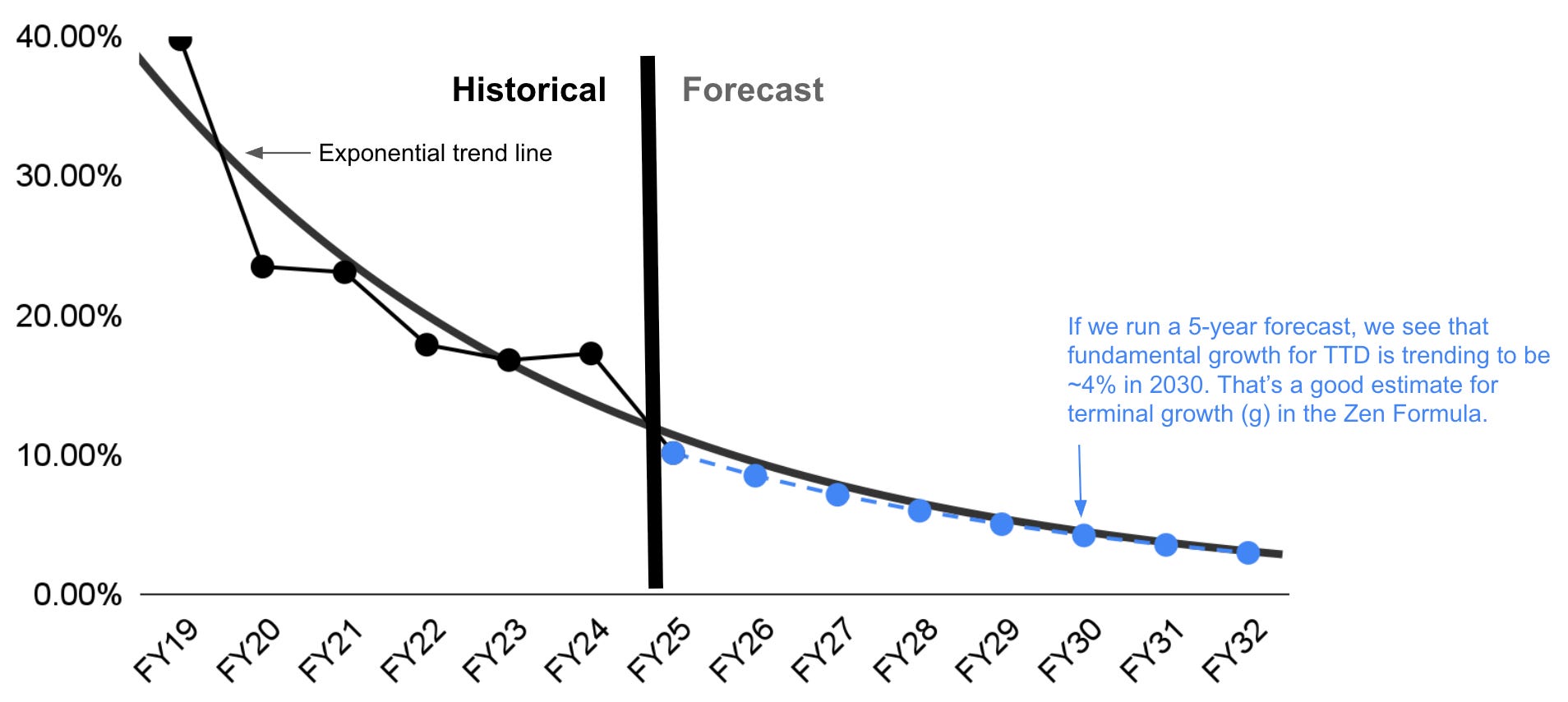

Fundamental growth (aka growth in operating profits) moves downward over time and toward GDP growth (around 3%) as markets and companies mature. The reason for this natural downward decay is simple: If a company could grow forever above GDP growth, it would eventually become the entire economy. That never happens.

Rearranging the value formula to see what’s happened to TTD

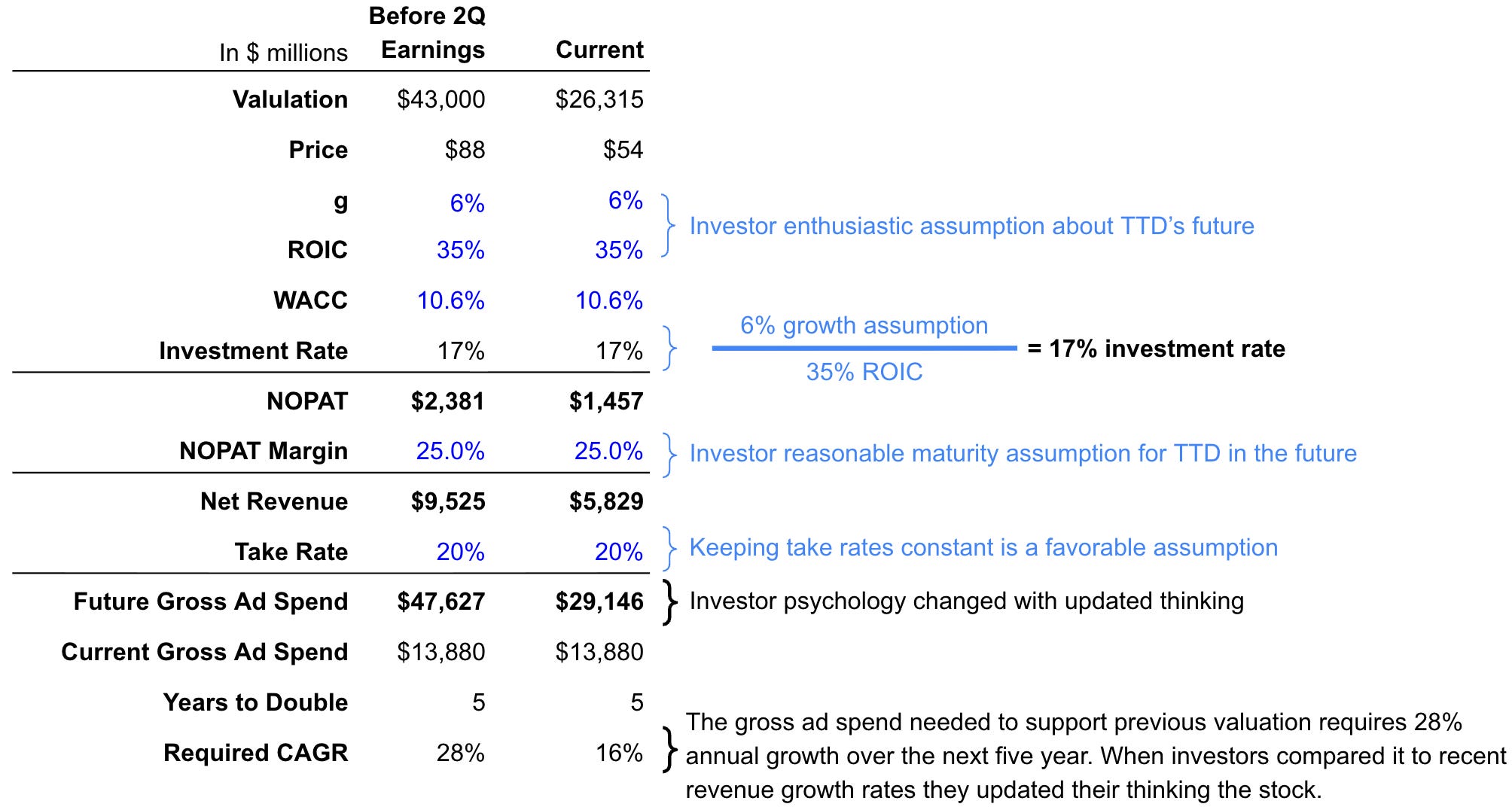

As we saw last week, investors interpreted TTD’s Q2 results/commentary, updated their thinking, and took their valuation down from $43 billion to $25 billion.

As far as Quo Vadis tries to understand the world, the big valuation drop means something changed with one or more of the four variables in the valuation equation. So, let’s look at the change from a different angle by rearranging the equation to solve for investor expectations around future operating profits.

In other words, let’s turn future operating profits into the protagonist (or antagonist) of the story by asking:

If the current market cap changed by ~40%, then how did they update their opinion on operating profits in the future (e.g. 5 years from now) if they hold the variables constant?

We know for sure that TTD’s market cap changed from $43 billion to $25 billion. That’s a known value.

We also know TTD’s cost of capital is 10.6% noting that beta has decreased over the past year from 1.70 to 1.35.

When it comes to ROIC, let’s say investors look at Google and Meta as the gold standard in the ad space. They consistently generate top-end ROIC around 45%. Over the past several years, TTD has been the darling of public adtech companies by consistently beating earnings and expectations for thirty quarters. TTD’s average ROIC since 2019 is ~18% and its trailing twelve-month ROIC is 25%. With that backdrop in mind, we think it is reasonable for investors to expect TTD to reach ~35% ROIC over the next few years.

That leaves us with having to model out fundamental growth at a future “terminal” point in time, like 5 years from now. Generally speaking, terminal growth rates fall in a 3% to 6% range. The higher the growth rate, the greater the valuation. For instance, P&G is 187 years old, went public in 1890, and is about as mature as a company can get. Its fundamental growth rate will always be close to annual GDP growth rates of around 3% to 4%. For The Trade Desk, it’s still a young company, so we think investors bake in something on the higher end around 6%.

With our best-guess variables in place, we can see how investors updated their thinking after Q2 earnings. Before TTD’s quarterly results at a $43 billion valuation, investors foresaw operating profits growing to roughly $2.4 billion around five years down the road.

After Q2 earnings, investors repriced the company to $25 billion, which implies they reduced their estimate of future operating profits (cash inflows) to around $1.5 billion, all things being equal.

Bringing it home with operating profit margins and gross ad spend

This is where the rubber meets the road. Operating profits in FY24 were 11% averaging 12% since 2019. On a TTM basis, Trade Desk’s operating margins are edging toward 13%. That leads investors to ask:

“What kind of operating profit margins can Trade Desk manage to create over the coming years?”

What do our gold standard comparables say? Google consistently generates ~30% margins, and Meta does a little better. When investors listen to TTD’s earnings calls, they hear two key themes: 1) Trade Desk competes with Google and Meta for ad dollars; and 2) The premium [open web] internet purportedly gets more overall attention than the biggest walled gardens, but the platform giants continue to attract more ad dollars.

With that backdrop in mind, it seems reasonable to conclude that optimistic TTD investors believe the company will figure out a way to generate ~25% operating profit margins in the coming years. For example, TTD already outperforms most peers in net revenue per employee at ~$750K/employee. By implementing an all-hands-on-deck AI productivity initiative aiming for $1M/employee, along with trimming down stock-based compensation expense, the company can control its destiny and get to 20%+ margins.

Breaking it down

With the above assumptions in mind (recapped in the table below), investor sentiment before TTD’s earnings last week implied future net revenue would mature toward $9.5 billion ($2.4 billion operating profit ÷ 25%).

If (and this is a big if) we hold future take rates constant at 20%, that means TTD would need to find $48 billion in gross ad spend. From a scale perspective, that’s a magnitude jump from the $13.5 billion expected in FY25.

Put another way: In the recent quarter, gross ad spend grew 19% YoY, but would need to grow by 28% annually to meet investor thinking where it was a few days ago. When investors revised future operating profit potential downward to $1.5 billion, they implied TTD’s gross ad spend potential was closer $29 billion, which translates to a 16% annual growth rate over the next five years. In essence, investors realigned new assumptions with new data.

Where to play next to find a sigmoid curve

All markets and businesses go through a life cycle of inception, growth, maturity (e.g., when fundamental growth settles around GDP growth), and then decline. When management sees a maturity plateau on the horizon, they try to find the next new big market and leverage their foundations built over the years to renew growth. That’s a sigmoid curve effect.

That’s where it appears Trade Desk stands today, but the future is bright. If there was ever a time for management to use McKinsey’s fall-back mantra — “we have a huge opportunity, it’s not going to be easy, we have a plan to get there” — this is it.

We see three blue oceans where they can do just that, and we think about it in terms of buy, build, or partner (in that order).

Let’s start backward with partnering and rule it out as a growth strategy. TTD already has hundreds of partners integrated in its ecosystem for important strategic reasons and/or for revenue share agreements. Partnering is important, but not a recipe for the kind of sigmoid growth that supports a higher valuation.

What about build? Yes, Trade Desk has a DIY culture, and it’s worked great so far. However, with AI changing everything, in tandem with the open web display ad space reaching maturity, while other areas like CTV are either locked behind walled gardens or highly competitive, the case for building is likely too slow. If we think about the case for building in terms of timing, difficulty, and impact, it tends to take longer than planned(more expensive), it tends to be more difficult (more expensive), and the planned impact is always at risk because the ad world changes so fast.

That leaves buying growth. Even better is buying into category ownership in a blue ocean space. We see three categories for TTD to invest in:

As web page eyeballs decline in favor of GenAI experiences, a brand new growth category opens up. This is where companies like Kontext ($10 million in seed funding, highly advanced tech) and OpenAds play. When you play here, you’re playing in the evolving search space. That’s a massive opportunity.

Social ad experiences are going beyond walled garden business models. Another category to invest in is how companies like C Wire are using targeting and creative AI to bring open web publisher inventory experiences closer to social experiences. Playing in the space matches TTD’s earnings call narrative to make an open internet on par or better than social.

Last but not least, there is CTV. The problem with Trade Desk’s current CTV strategy is not that it won’t work. It seems to be more about revenue replacement than growth (zero-sum strategy). A much better place to play for category ownership is in CTV virtual product placement. TTD already has an investment in Rembrand, whose founder/CEO (serial entrepreneur, Omar Tawakol) just joined TTD’s board. This is a blue ocean space with no category owner. The other player in the virtual product placement space is Ryff, which is also well funded with a long list of top production house partnerships that drive growing inventory avails. The “why now” for this space becomes evident when you realize how production companies in Hollywood are thinking ahead by shooting movies/series with white space to create variable product placement inventory, which in turn generates pre-paid budgets that fund new productions. The economic shift is fascinating when you think about it.

“They’re gonna try to tell you no, shatter all your dreams. But you gotta get up and go and think of better things.”

— Mac Miller

Disclaimer: This post, and any other post from Quo Vadis, should not be considered investment advice. This content is for informational purposes only. You should not construe this information, or any other material from Quo Vadis, as investment, financial, or any other form of advice.