#129: Novacap acquires IAS for $1.9B

All-cash transaction; Did Novacap get it right? Back-of-the-envelope estimates

Two new Season #2 pod interviews. My conversation with Andrew Casale started one year ago over lunch at The Smith in the East Village. If we had recorded our chat, which went deep into the economics of adtech, it would have been close to what we discussed in Episode #8. For example, Andrew shared his long-term optimism that AI will augment and “supercharge” publishing, while noting challenges like the rising “cloud tax” and the need for ad tech to evolve toward scalable, low-fee business models.

Episode #9 was with Sim Blaustein, general partner at 1745 Ventures, an early-stage venture capital fund spun out of Bertelsmann. If you’ve ever wondered what it’s like to launch a fund, get through all the formation stuff, and attract LPs, then our chat with Sim is for you. You can catch Sim on stage at the Advertising Economic Forum at Horizon Media’s HQ on October 7.

Check it out on Spotify or Apple.

Private Equity Novacap acquires IAS for $1.9B

“Integral Ad Science, or IAS, an adtech firm specializing in ad verification and measurement, has been acquired by Canadian private equity group Novacap in a deal worth $1.9 billion, the companies announced today.”

— AdWeek, Kendra Barnett

Here’s the back-of-the-envelope on how Quo Vadis values the deal.

Operating Profits

Trailing twelve-month Operating Profit (EBIT) for IAS is $73 million on $570 million in TTM revenue.

That makes for 12% EBIT margins. We like to see 20% EBIT margins or at least a path to 20%. IAS is on the right trend line with –16% in 2019 and 12% in 2024. Novacap clearly sees a path to 20% or more.

We assume a 27% cash tax rate on Operating Profits. You can defer and play it out with IRS tax rules all you want (with deferred taxes and interest expense tax shields), but the difference between reported taxes and cash tax estimates is usually material enough to dissect.

Return on Invested Capital (ROIC)

We estimate the current ROIC for IAS at 17%. Recall that GOOG (~45%) and META (56%) set the gold standard in the digital ad space.

Anything greater than the cost of capital is the first goal. The cost of capital for IAS is ~13% mostly due to a relatively high beta, so IAS passed that hurdle rate and will likely expand the spread under a private equity playbook.

From Novacap’s perspective, it appears they are eyeing a playbook to get ROIC closer to 30% given the $1.9 billion acquisition price.

Fundamental Growth

The hardest thing to deal with is fundamental growth. This is where IAS illustrates relative weakness with sub-3% fundamental growth rates. The rest of the public ad tech sector is somewhere around 3% to 5% (and negative for a few players).

Recall that the objective for managers is to generate fundamental growth rates greater than GDP for as long as possible. Global GDP growth rates in 2025 will be around 3%. Note that fundamental growth for Google and Meta is around 20% which is incredibly awesome.

The backward way to look at fundamental growth is to ask: “What proportion of post-cash tax operating profits does IAS invest back into new invested capital?” The answer is ~18%. That’s not much, relatively speaking. Google and Meta invest around 60% of operating profits back into the business which continuously drives an increasing stock price.

Simulating Novacap’s intrinsic value calculation and their bet on future operating profit growth

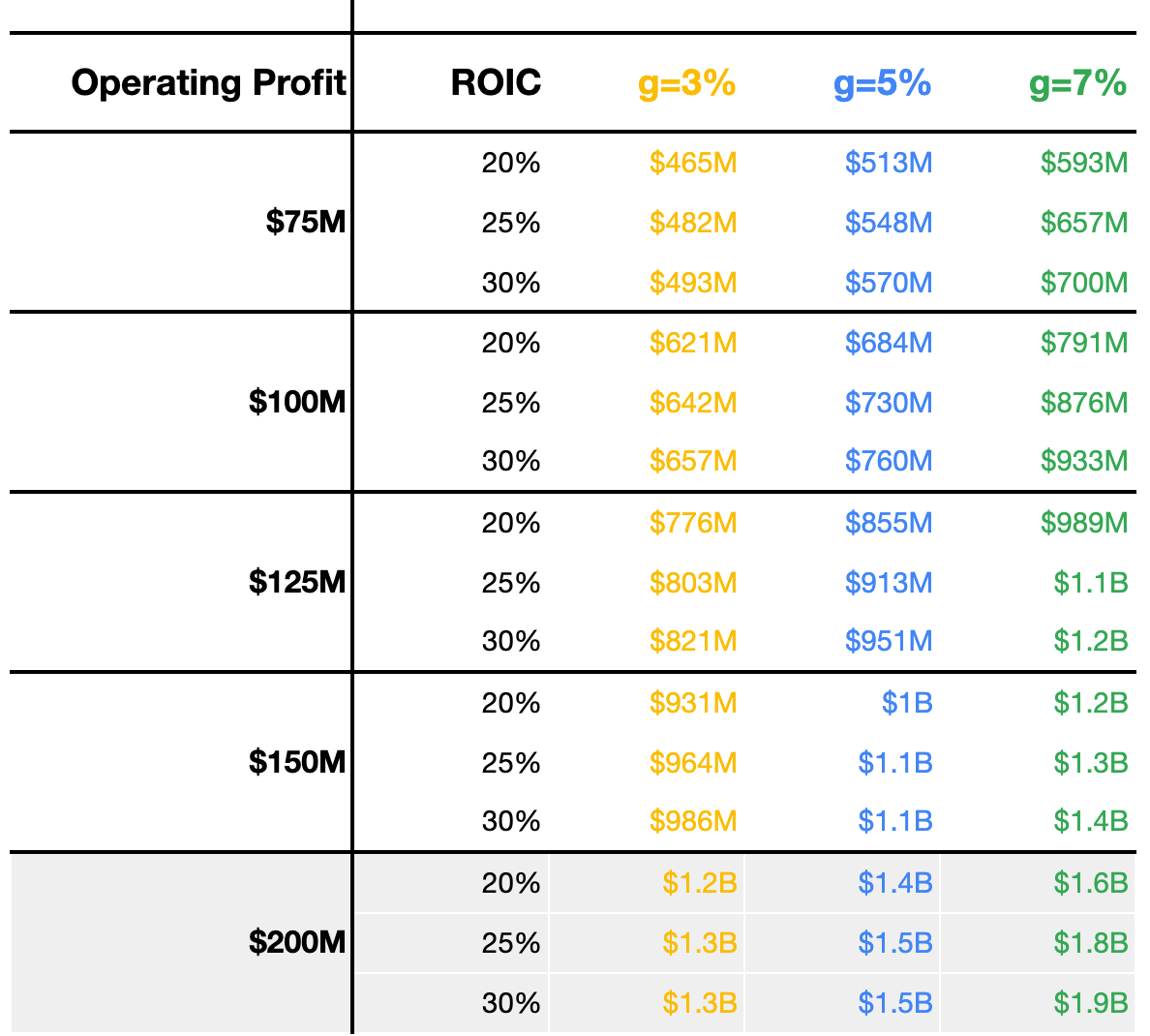

The matrix table below shows what IAS is theoretically worth in equity value terms (aka market cap) with different operating profit levels, ROIC, and fundamental growth.

From what we can gather, Novacap envisions operating profits growing by 2.5x from $73 million to ~$200M.

It appears that Novacap envisions 23% future EBIT margins and 20% post-cash-tax operating profits margins, which implies a future where IAS (measurement business + Publica) grows revenue from $570M to over $1 billion.

Current revenue growth rates average 20% per annum over the last five years, with 12% growth in the last fiscal period, 2023 to 2024. If annual revenue growth ticks up slightly to 13% with the new private equity playbook, it will take roughly five years to reach $1 billion. That seems plausible, possible, and probable.

The harder part will be boosting ROIC toward 30% and growing fundamental growth toward ~6% to justify the $1.9 billion buyout valuation.

Current IAS Equity Valuation

Let’s start with $73 million in operating profits with a 27% cash tax rate.

Current ROIC is 16%

Current fundamental growth is ~3%

IAS’s cost of capital is 13%

Given these drivers, the company is worth $660 million on a fair value “Charles Munger” basis. IAS was trading at $1.3 billion when Novacap offered a nice premium to get a deal done at $1.9 billion.

The Future

The future is unpredictable, but could be quite bright for Novacap. They clearly see something that we don’t. But we can try.

Valuing the company at $1.9 billion represents Novacaps’ intrinsic valuation. Let’s assume Bill Wise is right (and he usually is), saying that “the VAST majority of this take-private was funded by debt.”

If Novacap leveraged 70% (e.g., “vast majority “), that means they took on $1.3 billion in debt and paid $600 million in cash.

Assume an 8% debt rate on a 7-year term. If so, the annual payment is $250 million, split between interest expense of $100 million and principal payment of $150 million.

Making the interest payment off current ($144M) + expanding EBITDA is realistic.

Making the $150M principal payment off cash flow will be a bit more difficult.

However, if the private equity playbook includes cutting costs and increasing labor productivity to boost operating profit margins toward 30%, and if we assume a lower cost of capital (e.g., ~9%) due to the new debt vs. equity weighting, and also assume a healthy re-investment into new invested capital (e.g., $100M), then making that principal payment is realistic.

Let’s all this plays out over three years, culminating in a $1.9 billion exit. If so, Novacap generates a 47% internal rate of return and 3.2x return on cash.

We like it. As Brian O’Kelley also wisely said on LinkedIn:

“Option 1. Spin Publica. Great time to be in the ad server business with GAM [potentially] coming out of Google. Many ad tech and ad tech adjacent companies would pay good money for this. Bill Wise is waiting for your call. Take the money and buy the best asset you can afford that aligns with your core business. IAS will gain new resources to accelerate its AI-first roadmap, expand its CTV and programmatic offerings, and potentially integrate with Novacaps’ Cadent. I think being a private company will allow them to innovate faster in areas like agentic AI, CTV transparency, and real-time fraud detection - which we need!

A quick word on Publica

Back in 2021, IAS paid $220 million for Publica, “a CTV ad platform and working with many of the world’s biggest broadcasters, TV manufacturers, and over-the-top apps.”

In that quarter, IAS company reported:

“Revenue from our supply side customers increased $3.5 million, or 48%, primarily due to the acquisition of Publica.”

Annualizing $3.5 million implies $14 million in 2021 revenue for Publica. In other words, IAS paid 15x revenue.

Was it worth it?

It all depends. Global CTV ad spending today is around $30 billion. In the distant future, it will be roughly $175 billion as linear TV spending shifts to CTV eyeballs. If we assume ~$20 CTV CPMs and $0.25 CPM ad serving fees, and if Publica captures just 10% of the publisher market, that’s $220 million in revenue. Assuming a 5x multiple, Publica could be worth over $1 billion on its own.

As always, time will tell.

Disclaimer: This post, and any other post from Quo Vadis, should not be considered investment advice. This content is for informational purposes only. You should not construe this information, or any other material from Quo Vadis, as investment, financial, or any other form of advice.