#134: 3Q25 AdTech, MarTech, Agency Update

Equal-dollar portfolio update AdTech10, MarTech8, Agency6; Outcome-Driven Ad World and Advertiser Types

HOUSEKEEPING 1: Advertising Economic Forum is coming back to NYC on March 18 and 19, 2026. It’s where the business of advertising meets economics and finance. The forum is the first and only event experience that brings together the thinkers and doers who define and redefine value creation across the $1 trillion global advertising ecosystem. Founders, venture, private equity, corporate development, M&A, equity analysts, CFOs, and CEOs. Day 1 features our high-energy Founder + VC pitch competition hosted at Horizon Media. If you’re working on Agentic Agency, Agentic Creative, Buyer/Seller Agents, or Cognitive Commerce, and you’re bold enough to pitch your worldview thesis to a live audience on March 18, then get on our application list.

Day 2 is our “Davos of Advertising” experience, a closed-door, off-the-record forum where leaders reassess the probabilities of who’s winning and losing in the rapidly changing advertising market. If you’d like to attend, register your interest today!

HOUSEKEEPING 2: Last Media Dollar “Live” in London is on December 9 at Everyman Theatre in Borough Market. If you’re based in London/UK or happen to be in town on December 9, Quo Vadis is hosting our first LMD Live event. The courageous Cadi Jones will be playing the game live on stage as Tom Triscari plays color commentator. It’s an unscripted dialogue of media decision trade-offs in a room filled with inquisitive minds. The theatre only holds 100 people and is filling up fast. Quo Vadis subscribers get 25% off tickets with code LMD25.

3Q25 AdTech, MarTech, Agency Update

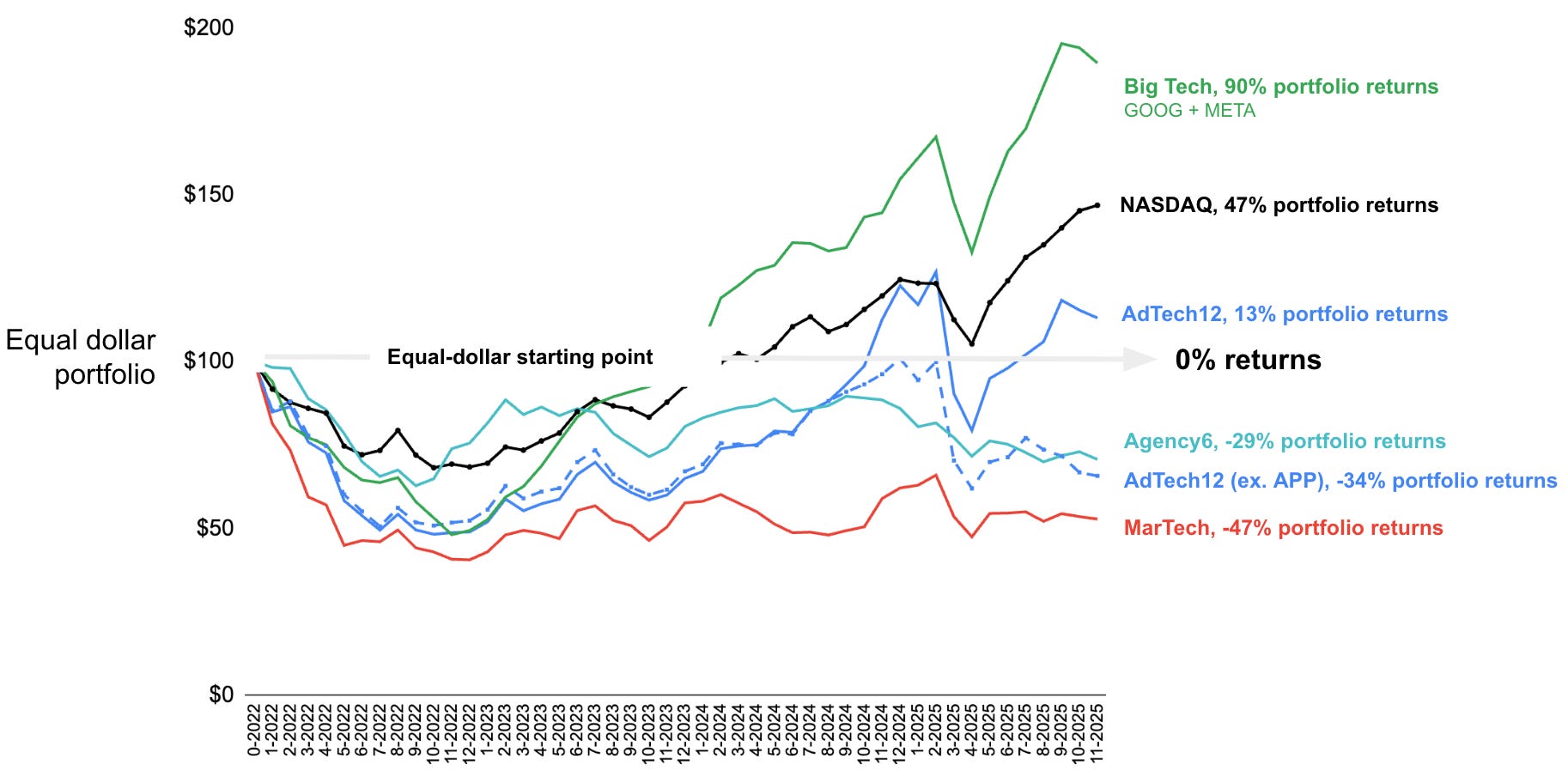

With 3Q25 earnings now in the rear-view, we can assess how public adtech names are holding up in a market increasingly shaped by channel shifts and sharper investor scrutiny. As a reminder, last quarter we rebuilt our equal-weighted portfolio beginning to start January 1, 2022, as a clean starting point since every company in our coverage universe was already public by then.

Here’s how it works using our AdTech12 portfolio as an example. You start with $100, divide it equally across 12 companies (see list below), buy shares in each based on the stock price on January 1, 2022, and hope to find alpha by beating the NASDAQ or S&P500.

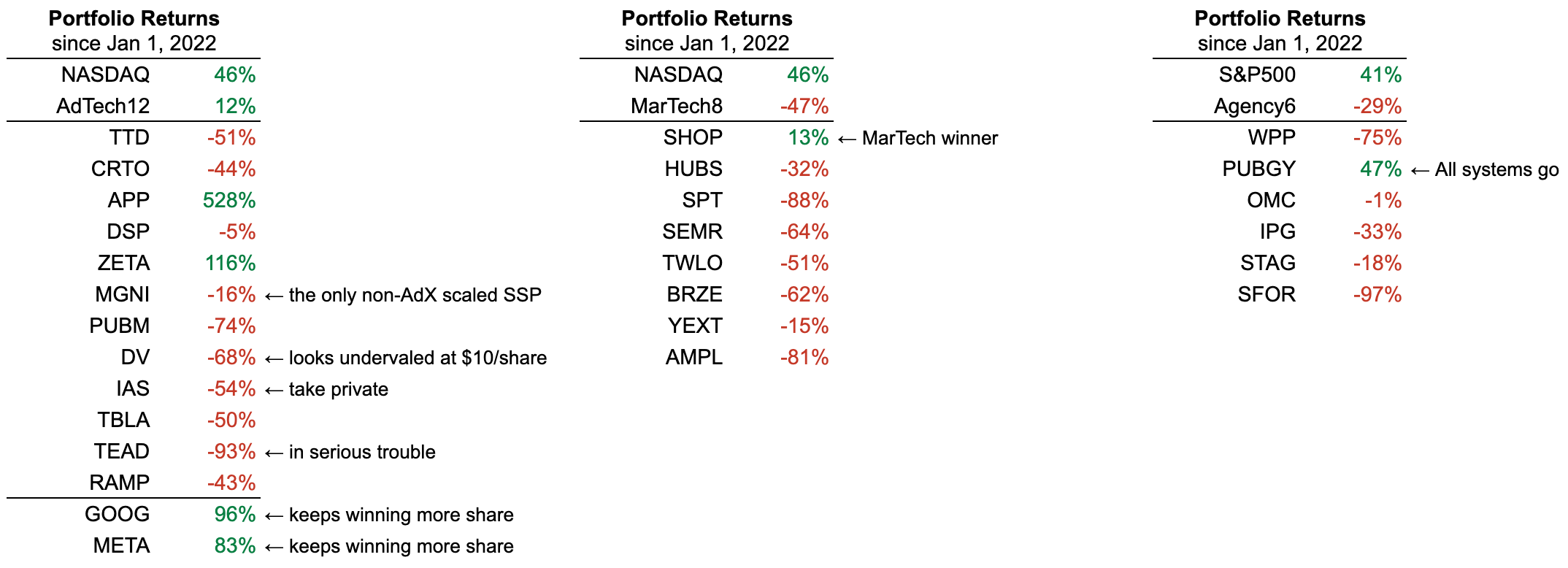

AdTech12

Our portfolio was up ↑6% in 2Q25 and is now up ↑13% as of 3Q25 reporting.

Peak returns happened in February 2025, performing in parity with the NASDAQ, but have since fallen off and dipped downward heading into year-end.

The AdTech12 includes: TTD, CRTO, APP, DSP, ZETA, MGNI, PUBM, DV, IAS, TBLA, TEAD, and RAMP. If we exclude APP, the AdTech11 would be down ↓34%.

When TTD was hot, it pretty much held up our entire portfolio, but it’s been rough sledding with dramatic shifts across the open web inventory scene. And with news like Omnicom Allegedly Pivoted A Chunk Of Its Q3 Spend From The Trade Desk To Amazon, the future is not going to be any easier. The Trade Desk is trading below a $20 billion market cap and heading toward our modeled fair market value closer to $10 billion or $20/share. That said, the company still has a massive opportunity, but it’s not going to be easy without a plan to get there. Management’s plan is unclear to us at the moment.

Besides AppLovin, Zeta is the only other positive performer across our portfolio.

The same $100 invested in a NASDAQ ETF would have returned 47% with less risk.

MarTech8

Our MarTech8 portfolio is dismal. SHOP, HUBS, SPT, SEMR, TWLO, BRZE, YEXT, and AMPL.

It was bad in previous quarters and getting worse, down ↓47%. Software used to eat the world. Now it seems that AI is eating SaaS.

Shopify is still the only bright spot, up ↑14%.

Agency6

Our agency portfolio consists of: WPP, Publicis, Omnicom, IPG (soon to be OMC-IPG, expected to close by year-end), Stagwell, and S4 Capital.

The agency world has been rough going, except for Publicis, up ↑48%.

WPP is still struggling, down ↓75%. WPP shares leaped amid takeover bid speculation from Havas, but Havas has denied the rumors. In other rumors, we’re hearing about internal infighting amongst the ranks at WPP. Similar to TTD, WPP still has a massive opportunity (for now), it’s going to be difficult anyway we cut it, and management’s 4-point plan is totally underwhelming. A better plan would be to simply say that:

“WPP is going to buy and create more of the best land (data) available. We are going to constantly enrich our land and rent it to clients (farmers) over and over again.”

Big Tech

We track two “Big Tech” players (Google and Meta ) in the ad space, with a third one on the rise (Amazon, see below).

Had you invested $100 in GOOG and META on a 50/50 basis in January 2022, you’d be up 90%.

Both Google and Meta had impressive quarters (again). We expect the good news to continue for both companies in the emerging outcome-driven ad world (more on that below).

Leaderboard Highlights

Teads (f/k/a Outbrain) looks to be in serious trouble after Outbrain acquired Teads and rebranded as Teads. Its market cap is down to just $75 million with $650 million in debt from the private equity-like deal.

We like DoubleVerify at $10/share. It does not take much in a discounted cash flow model to get to $20/share as DV’s M&A strategy is well-positioned for the outcome-driven world and agentic future.

IAS was taken private by Novacap. We covered our valuation thinking and deal rationale here.

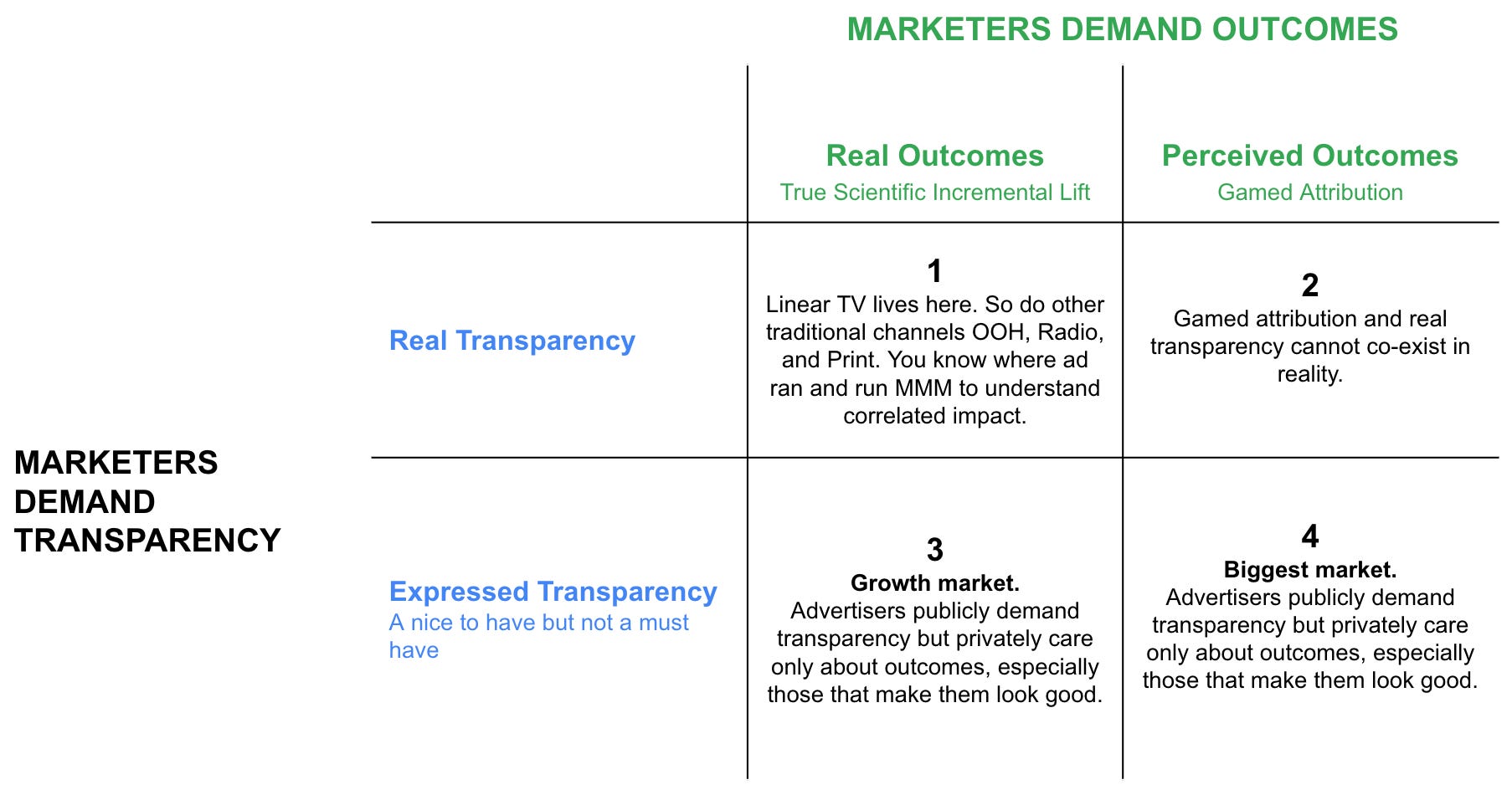

Outcome-Driven Ad World and Advertiser Types

Advertisers love to talk about transparency. They talk about it on stage in Cannes, at Possible, in trade press interviews, and on procurement checklists. But if you ignore the speeches and follow the money, a different truth emerges.

Transparency is a “nice to have,” but not a “must have” for the vast majority of marketers. The real market is in Boxes 3 and 4 below, where advertisers are free to express a preference for transparency but don’t behave as if they value it. It’s preference falsification in its purest form, and that’s okay. On hand, they say one thing because it sounds principled, and on the other, they spend on outcomes (real or perceived) because that’s the best place to look good. Welcome to the advertiser world 😂.

This is why black-box systems, such as Meta Advantage+ and Google PMax, continue to compound, and why principal-based agency trading continues to grow. The revealed preference of the market isn’t transparency, fairness, or control. It’s about performance, real or manufactured, and the political safety that comes with it.

Founder Tip: If you’re a founder of an adtech/mediatech startup, it is better to recognize this fact of life sooner rather than later, when you have to pivot into it to achieve going-concern status and keep your investors happy.

Interestingly, the only exception is Box 1. Linear TV is the third largest area of global ad spending (see Quo Vadis #130: Updated Media Money Flows) and incredibly resilient. However, with every passing day, it is shrinking as the growth engine of CTV. On traditional TV, marketers know where their ads run. On CTV, particularly across the growing long tail of thousands of streaming channels, they increasingly don’t know where all those CTV dollars are going. They are going to Boxes 3 and 4.

It is equally interesting to overlay the advertiser's long tail, ranging from large advertisers to SMBs and tiny advertisers. The deeper you go into the tail, the less transparency is demanded and the more outcome-centric the buyer mindset becomes.

Here’s a test to prove our thinking is realistic. Would you rather:

Spend $100K on a campaign that offers the amazingly angelic, crystal clear 100% transparency, and get $150K in outcomes?

OR

Spend $100K on a campaign and get $200K in outcomes?

If you’re a marketer speaking on stage at an industry conference, you’d obviously go with the former. But when you get off stage and sign the insertion order, you’d go with the latter, and you know it.

Our little test helps explain why Google, Meta, and Applovin are crushing it quarter after quarter. When you have the best mousetrap, the world will beat a path to your door.

Disclaimer: This post, and any other post from Quo Vadis, should not be considered investment advice. This content is for informational purposes only. You should not construe this information, or any other material from Quo Vadis, as investment, financial, or any other form of advice.

Same! But get them on stage, and they say the opposite: "measuring outcomes is the most important thing for us... We don't spend money on gamed attribution." Yet, they keep spending more money on gamed attribution :)

Love the part about demanding transparency. Working in ad tech since 2014, and I've never met a single client who would put effort into measuring real outcomes over being happy with the gamed attribution system.