#150: Publicis bought LiveRamp for a seat at the Identity Trade-Off Frontier.

Why the future value of advertising may belong to whoever pushes the Scale–Accuracy frontier outward the furthest and fastest

#CannesLions is around the corner! If you are interested or invested in the commerce media space, then join our string of events with Fluent and Landmark Ventures as part of your weeklong Cannes journey. You can RSVP here.

And if you’re interested in How Agencies Win in the AI Era: Automation, Intelligence & Growth join my exclusive breakfast session at Belle Plage Beach Club with John Kahn (Chief Transformation Officer, Digitas North America), Domenic Venuto (Chief Product & Data Officer, Horizon Media) and Jeet Singh (Founder, AtomicAds) exploring how AI agents and automation are reshaping agency models, media operations, and future growth. You can RSVP here.

Above Data Breakfast: If you’re interested in a beachfront breakfast with Above Data on how the data layer must evolve to support interoperable signals across advertising, then RSVP here.

Criteo Yacht Talk: On Wednesday in Cannes, check out Brian Wieser, Todd Parsons, and yours truly on Criteo’s yacht for our chat about how competing measurement models are redefining effectiveness. You can RSVP here.

C Wire Chill House: Besides my 1-to-1 chat with Sir Martin Sorrell on Sunday (see Fluent link above), we’ll continue our conversation at C Wire’s AdTech Chill House on Thursday morning. You can RSVP here.

Publicis bought LiveRamp for a seat at the Trade-Off Frontier

Let’s start with a simple question:

Did Publicis acquire LiveRamp because of its financial performance?

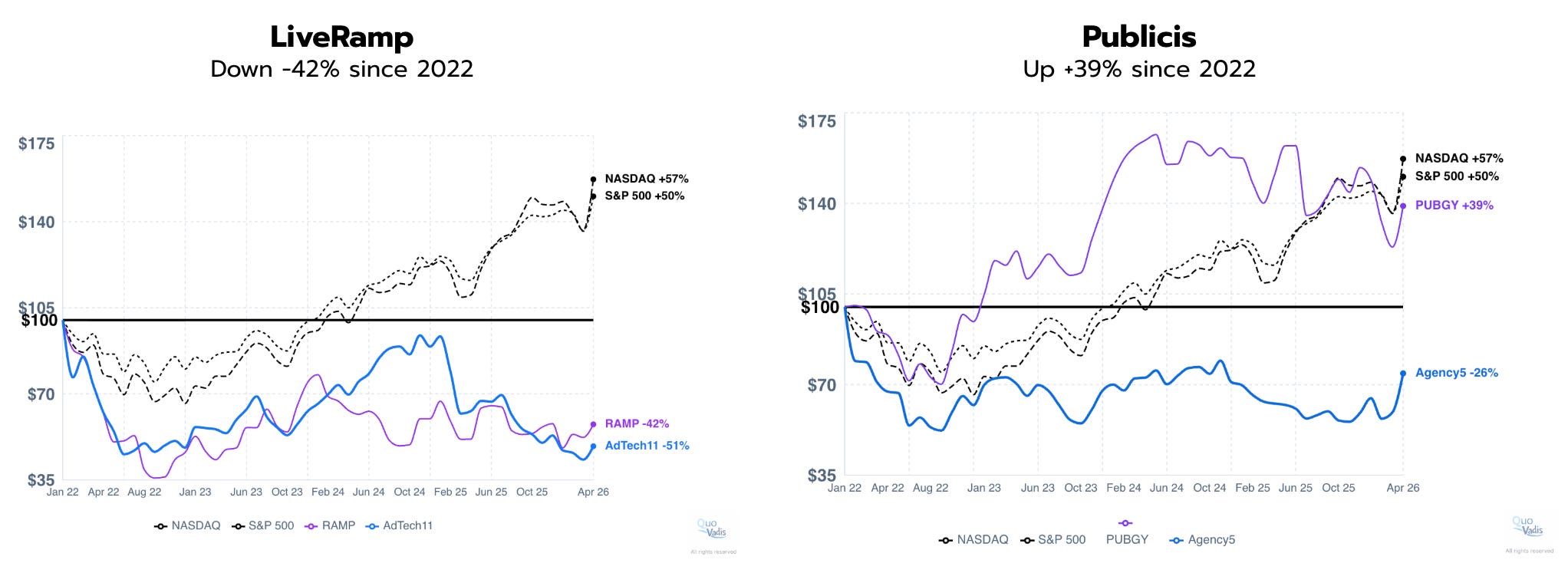

Highly unlikely. LiveRamp generated $813 million in revenue last year, representing 9% year-over-year growth (noting that RAMP’s fiscal year ends March 31). After years of struggling to achieve profitability, the company reached only modest operating margins two years ago (2% EBIT margin), followed by 1% last year and 10% this year. Notably, last year’s improvement was driven by a combination of moderate revenue growth with meaningful reductions in R&D, sales, and marketing expenses.

While LiveRamp has only recently achieved modest profitability, Publicis operates globally and delivers outstanding financial results. The company generated $3.1 billion in operating profit on $17 billion in net revenue (after pass-through costs), achieving an 18% operating profit margin.

Even with post-deal cost synergies (which could be material in LiveRamp’s case), the deal would not materially alter Publicis’ near-term earnings trajectory on a financial thesis alone.

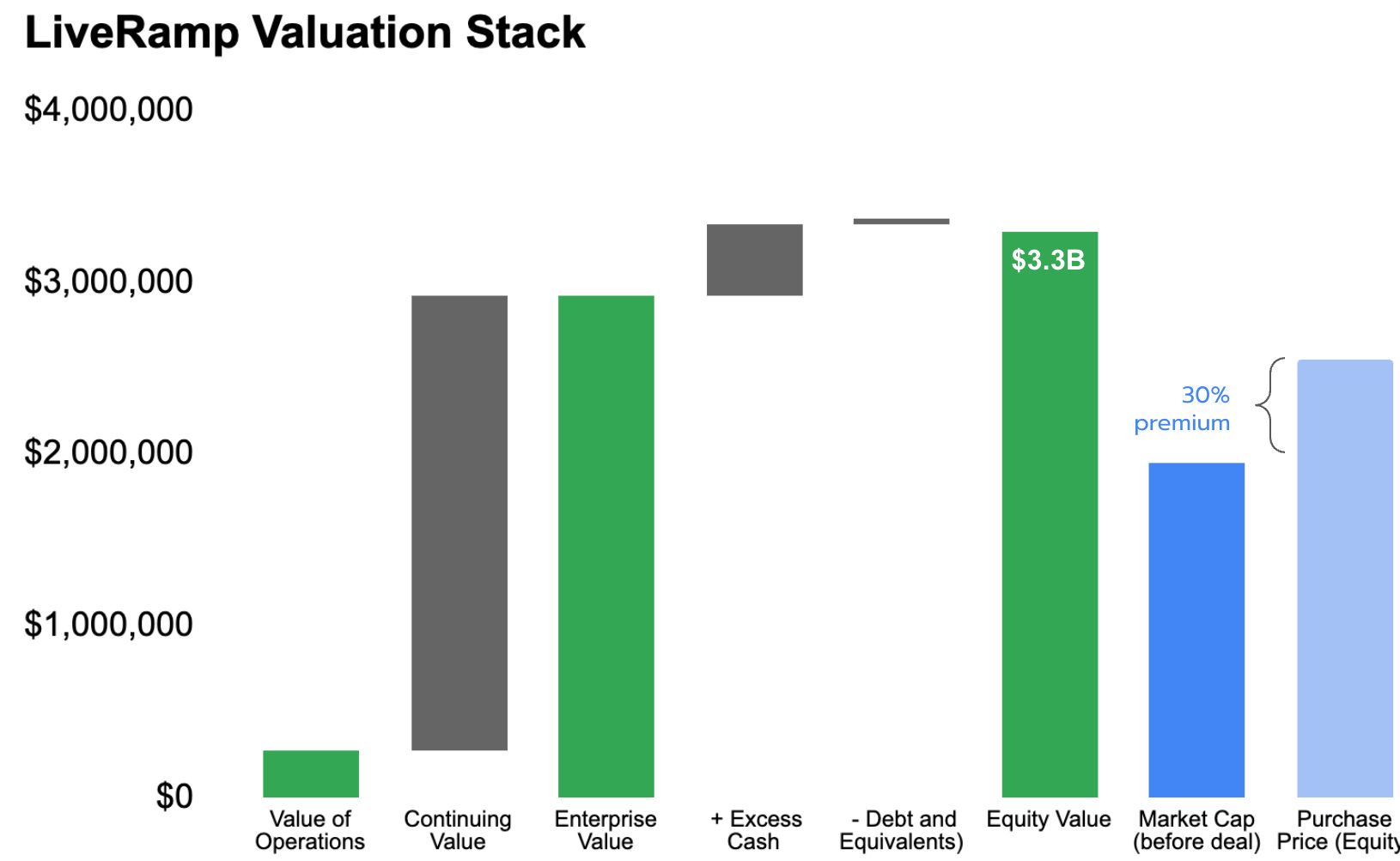

Even if we assume LiveRamp was able to grow its operating margins from 10% to 25% over the next five years under Publicis, and grow revenue at a 10% CAGR, and further assume that LiveRamp’s ROIC grows from ~0% to Publicis's 45% level, the financial value to Publicis is only $3.3 billion. While that’s more than 10% of Publicis’s ~$25 billion market cap, it's more like icing on the cake than the actual true value of the meal.

As Auren Hoffman mentioned on Martetecture’s podcast with Ari Paparo and Eric Franchi, that outcome would generate a 30% internal rate of return, which is still really good from a pure cash-out/cash-in perspective. If Publicis were simply playing out a private playbook, that would be a home run deal.

In 2022, Publicis reported having 3,620 “major” clients (see registration document, page 31). Even if we further assume half of Publicis clients convert into LiveRamp subscription customers over the next five years, our valuation model indicates the company would be worth $4.1 billion in equity value to Publicis, generating a really nice 67% IRR. But we think there is more to it than just a really good financial return.

Now let’s ask:

Did Publicis acquire LiveRamp to win new agency clients?

Perhaps. Even if LiveRamp’s product is a great puzzle piece for Publicis, we don’t think new client acquisition alone justifies the acquisition. Although it could be a meaningful competitive advantage to have differentiated data assets in new client pitches, we think the real value is in using the data infrastructure as a centerpiece to achieve a 10x return (or more) and gain a competitive leverage with walled gardens.

How about another question floating around LinkedIn?

Did Publicis ignore the obvious risk that LiveRamp may lose customers once neutrality disappears under agency ownership?

Almost certainly not. If we are right about the real reason why Publicis acquired LiveRamp, customer churn risk will not matter much. Moreover, Arthur Sadoun (CEO), Adam Berkowitz (Corp. Dev.), and the deal team at Publicis are very sophisticated and would have modeled churn scenarios during deal diligence. They undoubtedly considered the possibility that some customers leave because LiveRamp no longer sits outside the ecosystem as an independent “Swiss” intermediary, but dismissed frictional churn as a non-risk.

That said, a reasonable bear case could be made that Publicis knowingly accepted near-term churn as a cost of acquiring a more valuable long-term infrastructure asset. Using rough estimates, Publicis (~3,600 clients) and LiveRamp (~860 clients) likely overlap by ~35% or ~320 enterprise customers, leaving ~540 potentially exposed to churn from competing agencies or brands concerned about neutrality under Publicis ownership. Even if 30% to 50% of those non-overlapping LiveRamp clients were eventually lost, our 10x data infrastructure strategic thesis is a far larger win once the dust settles.

Data “Infrastructure” Assets are Trade-Off Curve

So, if Publicis understood limited financial upside from LiveRamp as a stand-alone business, as well as the aforementioned risks, and moved forward anyway, we think a more interesting question emerges:

What if Publicis believes the future value of advertising belongs to whoever pushes the industry furthest along the Identity Trade-Off Frontier?

In our view, Publicis has proven itself to be the agency with the winning hot hand, and it is now buying deeper control over identity and data connectivity with an eye to expanding the density of connections across its giant client ecosystem, which in turn stimulates data flows for which clients will pay high rents. If so, we think the acquisition is best viewed as a flywheel-mediated play.

The Identity Trade-Off Frontier

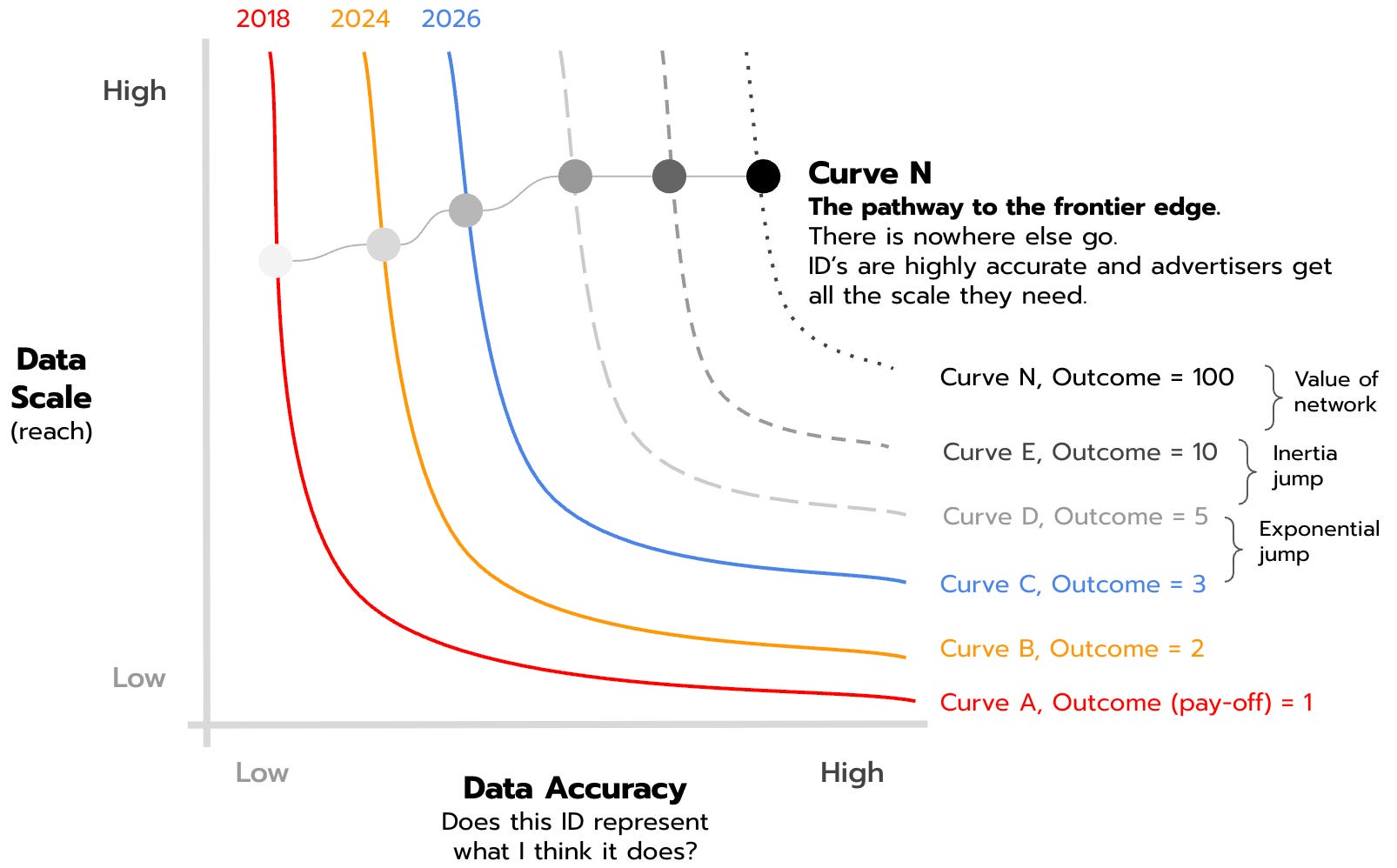

For much of digital advertising history, marketers lived on a data utility curve where scale (reach) of audience data can be interpreted as a trade-off with data accuracy (e.g., Does this ID represent what I think it does? If I am targeting females, is the person behind the ID really a female?)

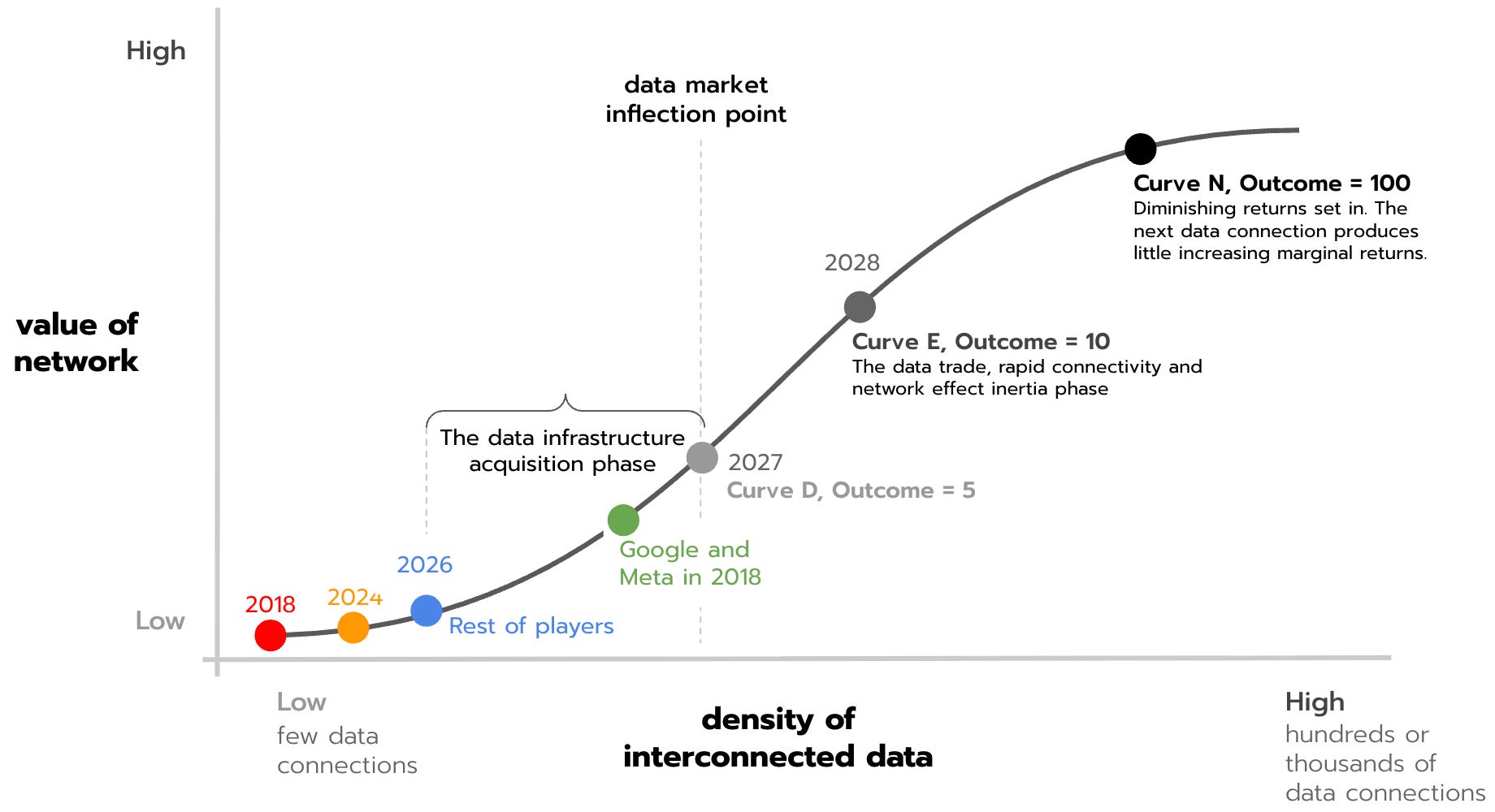

Curve A: Pre-2018, we lived in a third-party cookie-based industry that was mainly optimized for scale vs data accuracy. Truth be told, targeting in that world was slightly better than random. Cookies proliferated, third-party data exploded, and so did bad bots deployed by arbitrage actors to boost traffic and impersonate users. In that world from yesteryear, probabilistic identity promised precision by stitching together impressions, devices, platforms, and intermediaries. The scale was enormous, but identity precision was mostly overstated. Brands could buy enormous reach at relatively low cost, but much of the underlying connectivity was highly probabilistic and uncertain, resulting in poor outcomes (aka utility payoffs).

Curve B: Identity Infrastructure Pushes the Frontier Outward: Then the world changed. Privacy regulations accelerated, cookie deprecation began, the push for logged-in authentication expanded, first-party data became strategic, and identity graphs gained importance.

On the one hand, this new state did not eliminate uncertainty about data accuracy. On the other hand, it simply replaced lower-confidence probability with higher-confidence probability. By 2024, accuracy had improved, the data frontier had shifted outward, and a better payoff materialized with higher utility for advertisers.

As the frontier expanded, any company positioned closest to authenticated data (LiveRamp, Walled Gardens), transaction signals (Amazon, Criteo), and deterministic identifiers (Walled Gardens) possesses an economic advantage.

Curve C: Competing with Walled Garden

While the rest of digital advertising was dealing with Curve A in 2018 (and before), Google and Meta were already at Curve C in 2018 (and likely beyond), delivering rich outcomes with the highest utility.

By 2026, identity and data infrastructure players like LiveRamp, Trade Desk UID2.0, ID5, MediaWallah, Above Data, HighTouch, Optable, Anonymized, Growth Code, and others entered Porter’s 5 Forces as new entrants with innovative solutions that addressed the audience-targeting job in a new way.

Today, when industry practitioners talk about the new era of “outcome-based” advertising, Quo Vadis interprets Curve C (2026) not as proof that the industry has arrived, but as the inflection point separating the old world from the emerging one. Curve C represents the moment when outcome-based advertising becomes economically viable at scale and charts a course for continued high-speed improvement over the coming years. Whether advertisers spend media dollars on Walled Gardens or the Open Internet, they can achieve large-scale reach with more accurate identity data to increasingly get the outcomes they seek.

In essence, a seemingly small linguistic change from “media buying and optimization” to “outcomes-based” represents the largest economic transition in advertising history since the Internet’s first ad in 1994. When outcomes become the objective, all future competitive advantage for all players in the advertising business depends on hooking yourself to the next trade-off curve on the frontier.

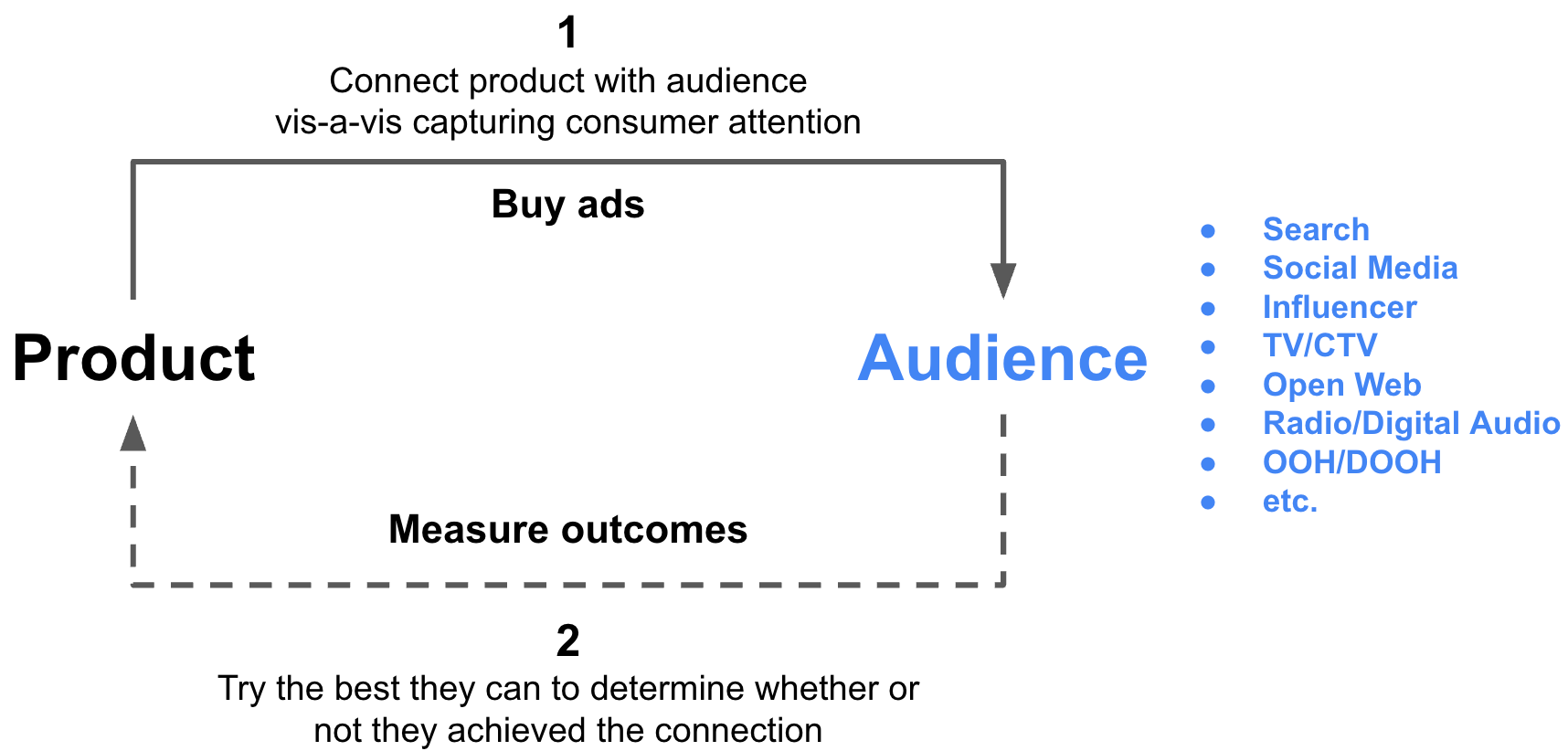

The frontier becomes the prize

The advertising job, in its simplest form, is about doing the best you can to connect your product with an intended audience and capture attention maximization (aka salience) through media buying and creative, and then determining (measuring) whether the connection happened (outcomes).

From our perspective, outcome-based advertising is about an ecosystem getting materially better at both, which manifests in the outward shift from the current trade-off curve to the next frontier curve. The inertia driving the frontier forward is about data connectivity.

We think the trade-off curve model helps explain why Google, Meta, and Amazon have been years ahead of the Open Internet, but perhaps not for long. The walled gardens are “walled” because they are control points for identity, O&O media, commerce, logged-in users, and transactions. Whatever curve they are on today does not matter as much as the firm foot they always seem to have in the next frontier.

As for the rest of digital advertising, everyone is racing toward data and identity infrastructure ownership because that is where advertisers will pay the most rent. Agencies, retail media, identity firms, data infrastructure companies, DSPs, SSPs, PubTech, and publishers all need to get well-positioned today, as they know future value creation will occur on the next frontier curve.

The Density of Interconnected Data and Network Value

Owning data alone is not enough. The future belongs to market makers who enable and coordinate data connectivity between data trading partners.

For example, let’s say you’re in London and the forecast calls for wind and rain, so you take your umbrella to stay dry. Before you leave your house, you hesitate and take a second umbrella just in case the first one breaks in the wind. Before you jump on the tube, you stop at a kiosk and buy a cheap umbrella just in case you lose the second one. Now you’re walking around with two hands and three umbrellas. Each successive umbrella has decreasing marginal utility. If you were maniacal enough to grab a fourth umbrella, it would have zero marginal value.

Data is different. When you connect one data source or signal to another, not only do they both increase in value, but the combined “networked” value is even higher. For instance, let’s say two ID data sets, A and B, are both 50% accurate. When combined, A is 60% accurate, B is 60% accurate, but AB together is 75% accurate. That’s increasing marginal returns.

Yes, at some point, diminishing returns will kick in, with the nth data set providing minimal margin gains. For illustrative purposes only, the chart above maps our trade-off curves to the concept of density of interconnected data and shows how diminishing returns set in.

From the advertiser’s perspective (clients of agencies like Publicis), most proprietary data remains connected to only a small subset of potential datasets, even as brands seek to operate closer to the frontier. If infrastructure providers like LiveRamp can accelerate the creation of new connections across fragmented consumer, commerce, retail, and media data, the resulting increase in interoperability should raise the value of that data through improved measurement, activation, and outcomes.

From the perspective of agencies and other data infrastructure players, the more data connections they can enable as market makers, the more data will flow. The more data flows, the more rent can be charged for making it happen.

How The Least-Worst Alternative Can Become the Most Valuable Position

Since Publicis' announcement on May 17, we've found it interesting that so many people in the industry dislike Liveramp. Auren Hoffman mentioned this more than a few times on Marketecture’s pod.

Although it’s unintuitive, maybe that’s what makes LiveRamp so valuable. The product might not be great and has been totally underinvested in over the past 10 years, but it does have a strong position (~70% market share) as the least-worst alternative outside the walled gardens.

For all competitors, substitutes, and new entrants in the data or infrastructure game, the best strategy is to be the next best, least-worst alternative (if that makes sense). The more this happens, the further the industry moves outward on the frontier.

In our view, the negative sentiment murmured on the street is evidence of a strong strategic position, not weakness. And as you should expect, the data industry is not the first or last to discover that the least-worst infrastructure assets are rarely loved. Instead, they are tolerated, criticized, and relied upon until, one day, the market realizes that the least-worst alternative is an indispensable control point.

For instance, traders complain about Bloomberg terminals, yet they are indispensable. Advertisers and networks complain about Nielsen, yet it’s still the benchmark currency. Consumers complain about credit bureaus, but they need them to get loans. Businesses complain about SAP, but don’t switch to alternatives. And adtech people complain about LiveRamp, yet its integrations persist.

LiveRamp is not valuable because participants love using it. It is valuable because enough parties connect through it, albeit reluctantly in many cases. That said, whether there is reluctant connectivity or not, we assume Publicis sees that the density of interconnected data increases data flows, which in turn increases its economic importance. As Publicis economic importance grows, it will attract more data connections, more rents, and the loop compounds.

If that sounds less like software and more like railroads, payment networks, telecom infrastructure, and electric grids, then now you understand how we think Arthur Sadoun is valuing LiveRamp. Publicis did not acquire an identity company. Instead, they acquired a market-making data-connectivity control point to extract their fair share of future advertising rent in exchange for delivering superior outcomes at the edge of the Identity Frontier.

Viewed through this lens, LiveRamp looks less like an identity company and more like a transmission network or data exchange layer. Along with other Publicis assets, LiveRamp is a mechanism through which advertisers, publishers, commerce platforms, retailers, and media owners can increasingly connect information. For Publicis, it’s not about how much revenue LiveRamp can generate as a stand-alone business. The value creation is about how much future economic activity can be enabled through connected data and controlled by Publicis.

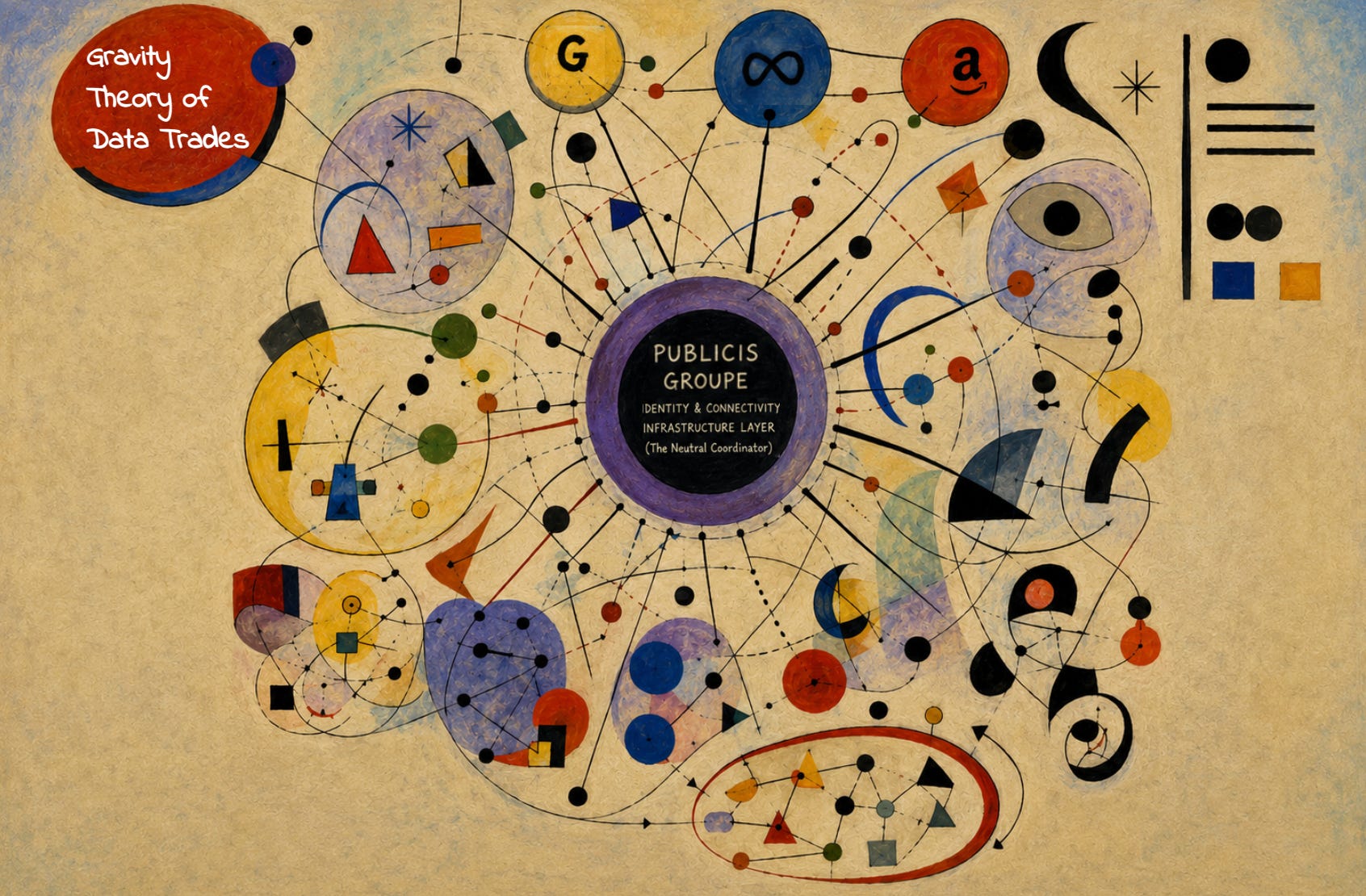

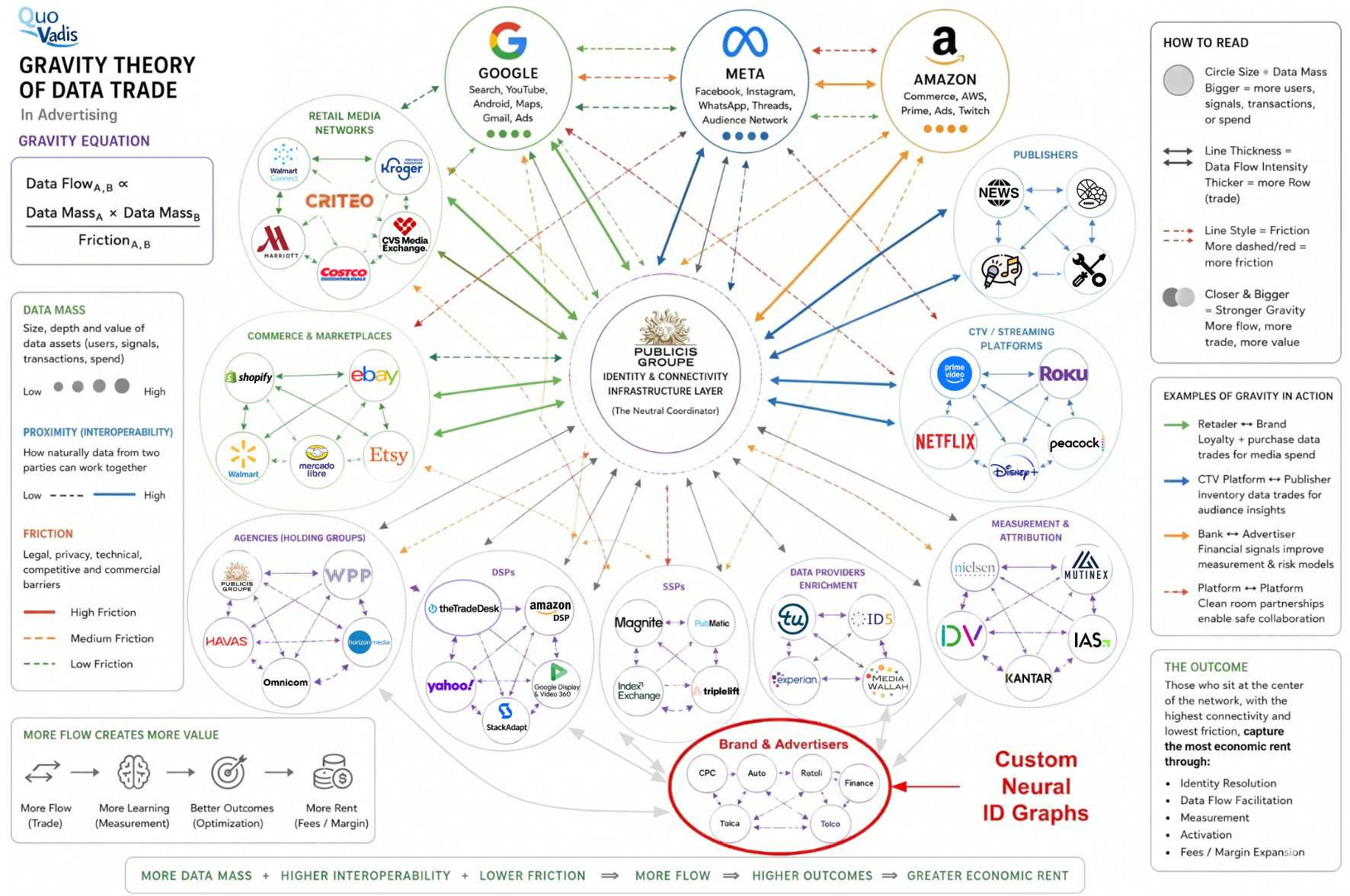

Gravity Theory of Data Trade

Economic theory offers another lens called the Gravity Theory of Trade. This concept was first proposed in a highly cited 1985 research paper based on Newton’s theory of gravity, known as E = MC^2.

Newton stated that every particle attracts every other particle with a force proportional to the product of their masses and inversely proportional to the square of the distance between their centers.

The Gravity Theory of Trade holds that trade between two countries increases with their economic mass and proximity. For example, the US and Canada are large economies that share a long border, so their trade volume is enormous. Fiji and Mozambique are small economies and far apart, so trade volume is low.

In subsequent economic research, concepts like “friction” were introduced. For instance, while the US and Canada are large economies and close to each other, the current political environment has introduced competitive friction and reduced trade.

If we are correct about Publicis’s worldview, then advertising is about to enter a very exciting phase through bilateral data trades.

Our proxy formula states that data mass is achieved through users, transactions, audiences, spend, and/or signals. In the denominator, Competitive Proximity x Friction is the relationship between friendly cooperation and pure competition, with the “frenemy” concept somewhere in between.

Our intentionally busy chart proposes an emerging Gravity Theory of Data Trade across the advertising space, with Publicis right in the middle. If a $2.5 billion asset can be converted into $25 billion of value creation for Publicis shareholders, this is how we see that materializing.

The central idea illustrated in the chart is that data flows among participants (agencies, DSPs, SSPs, publishers, retailers, platforms, brands, measurement firms, etc.) much like trade flows in economics. Larger participants with more data, closer competitive proximity, and lower friction will tend to exchange more information with each other.

Each circle represents a participant or ecosystem. Circle size approximates data mass (users, transactions, signals, spend). Line thickness represents data flow intensity, while dashed or colored lines represent friction (privacy constraints, competitive incentives, technical barriers, regulation).

Smaller sub-networks illustrate how trading already occurs within groups (e.g., agencies with agencies, SSPs with SSPs, retailers with retailers) before and/or concurrently flowing outward into the broader ecosystem.

At the center sits an identity/connectivity infrastructure layer, representing the intermediary coordinating data exchange. In this example, Publicis + LiveRamp acts as the hub. Every time a byte of data moves through the market maker, Publicis’s cash register rings.

At the center sits an identity/connectivity infrastructure layer, representing the intermediary coordinating data exchange. In this example, Publicis + LiveRamp acts as the hub. Every time a byte of data moves through the market maker, Publicis’s cash register rings. There are also independent identity providers, such as ID5 and others, that have become increasingly valuable because they reduce friction and improve interoperability (connections) among otherwise fragmented participants, enabling more trade without touching the underlying media flows.

For advertisers, whoever owns pipes that help advertisers get their best seat at the data trade table is in just as good a position as Publicis is today. The red-highlighted section at the bottom of the chart suggests a new state in which agencies (or other party) assist advertisers in enhancing and owning their custom neural identity graphs, thereby increasing the density of their own connected data. This is precisely what makes companies like MediaWallah so valuable.

If our conclusions are correct, Publicis is betting that the next era of advertising belongs not to those who buy media most efficiently, but to those who own the infrastructure that helps move the frontier. If that is true, the LiveRamp acquisition will eventually be remembered as something much larger than an M&A transaction. It will be remembered as a very smart bet that Arthur Sadoun placed on the future data trades.

Who has the largest data mass? Which participants sit closest to the center of the data flow? Where is friction highest today vs. tomorrow? Which new connections would increase flow? Who captures economic rents as data trade expands? These questions and many more will be answered over the coming months and years.

Other good reading on this topic:

Publicis + LiveRamp: Big Positive For Publicis, Big Impact for Rest of Agency, Ad Tech and MarTech Sectors (Madison & Wall)

Publicis and LiveRamp: Additional Considerations On Combination (Madison & Wall)

Who Owns the Pipes Matters (Keith Petri)

Disclaimer: This post, and any other post from Quo Vadis, should not be considered investment advice. This content is for informational purposes only. You should not construe this information, or any other material from Quo Vadis, as investment, financial, or any other form of advice.

Thanks Erez. Two thoughts come to mind:

1) When AI is good enough, predicting outcomes become obsolete because the outcome it self is created.

2) Upper funnel advertises don’t care about incremental gains like performance advertisers do. They are incentivized and motivated to not lose what they think they already have (loss aversion). It’s like inverse incremental if that makes sense where ROI can still be calculated/estimated.

Thought this was great, giving it a shout in our newsletter tomorrow!