#156: Bending Spoons IPO

Modeling the Path to $10 Billion Revenue, 40% ROIC, and a $21 Billion Valuation

Bending Spoons is a fascinating business model with what appears to be a next-level management team. The company, whose mission is to acquire and improve well-known products like Eventbrite and Vimeo, went public on the NASDAQ sixteen days ago, raising ~$933 million in fresh acquisition capital (net proceeds) and reaching a $25 billion market cap. As of yesterday, Bending Spoons’ equity value has settled downward at ~$21 billion.

The word on the street is that target companies love working with Bending Spoons because of its “in-the-trenches” management team, which is a huge advantage for inbound targets (deal flow) looking for a better home at fair prices.

Bending Spoons’ management believes startup success is heavily influenced by luck, particularly in achieving product-market fit. In their view, great founders often fail while mediocre ones succeed because they happen to build the right product at the right time. By contrast, they also believe operational excellence is a learned capability (not luck).

With those two tenets in mind, management believes that many successful digital businesses are well-positioned but poorly managed, thus creating an opportunity for exceptional operators to acquire, optimize, and dramatically improve them.

Based on these insights, and to prevent future success from depending on luck more than necessary, management has devised two strategic objectives:

Build the perfect operating machine. We would put our hearts and minds into becoming the best possible operators of digital businesses. The better our operating machine became, the more a digital business would gain as part of Bending Spoons versus as a standalone entity.

Compound capital through acquisitions. Operational excellence would unlock an opportunity to grow efficiently through acquisitions. We would, in effect, be outsourcing the search for product-market fit, while directing all of our energy toward excelling at everything else.

Given the current $21 billion equity value, Quo Vadis is interested in modeling the company's historical financial performance and forecasting what the future will need to look like to justify the enthusiastic market cap investors have assigned to the company. In other words, what we are asking is: What needs to be true in the future in terms of revenue, after-tax operating profit margins, and return on invested capital in order to make the current market cap true?

Bending Spoons Business Model

Targets: Before we do that, let’s quickly cover Bending Spoons’ business model. Rather than competing to build the next great app, the company acquires established digital brands with loyal users, recurring revenue, and operational complexity that others view as liabilities. Bending Spoons likes to target subscription or recurring revenue, a strong consumer or SMB brand, slowing growth, public-market disappointment (is public adtech next?), and/or an overly large engineering or operating cost base with meaningful opportunities to introduce AI and automate operations.

Playbook: Bending Spoons management then applies a centralized operating system that combines a playbook of AI, engineering, data science, and disciplined capital allocation to simplify operations, improve product economics, and generate more cash from the same assets.

Strategy: Their strategy resembles that of a permanent acquirer more than that of a traditional private equity firm, in which targets are acquired to compound on their own and contribute to the whole, rather than being fixed and flipped. If successful, Bending Spoons' enduring competitive advantage rests on a repeatable operating system that can continuously acquire, integrate, and optimize software businesses at scale.

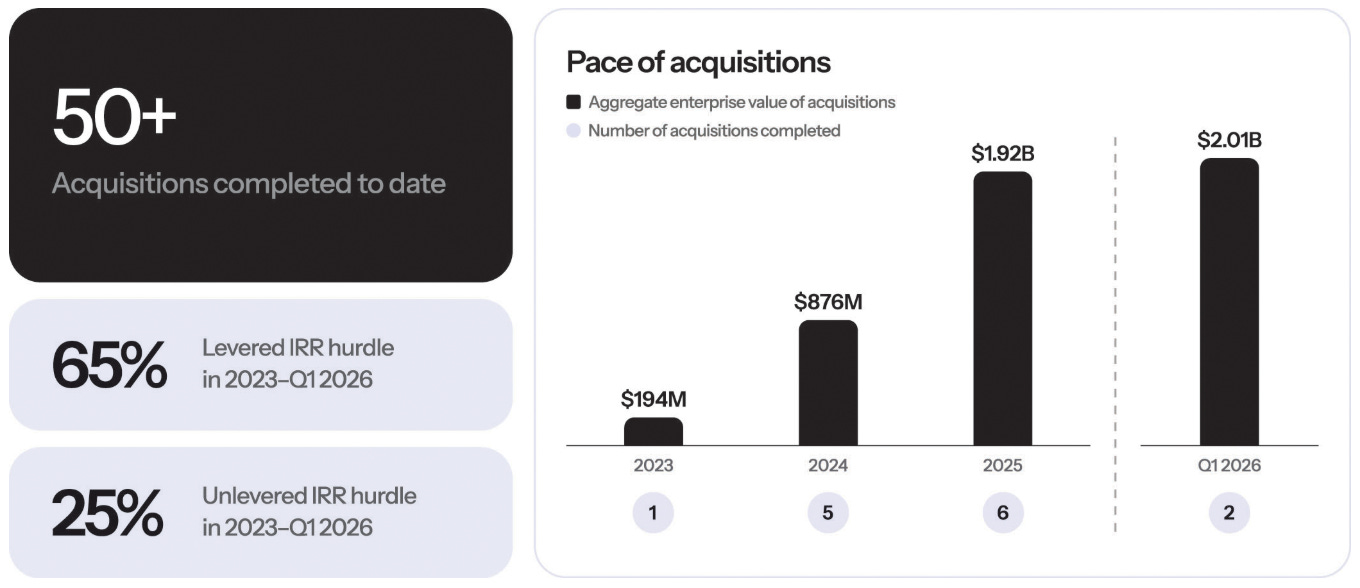

History: Bending Spoons has completed more than 50 acquisitions over the past 13 years, evolving from buying a $10,000 app to pursuing multi-billion-dollar takeovers including Evernote, Meetup, WeTransfer, Brightcove, Vimeo, AOL, Eventbrite, Harvest, and Tractive, with a combined 1+ billion registered users, 400+ million monthly active users, and 7+ million monthly paying customers.

Recent Target Average Valuation (Sample):

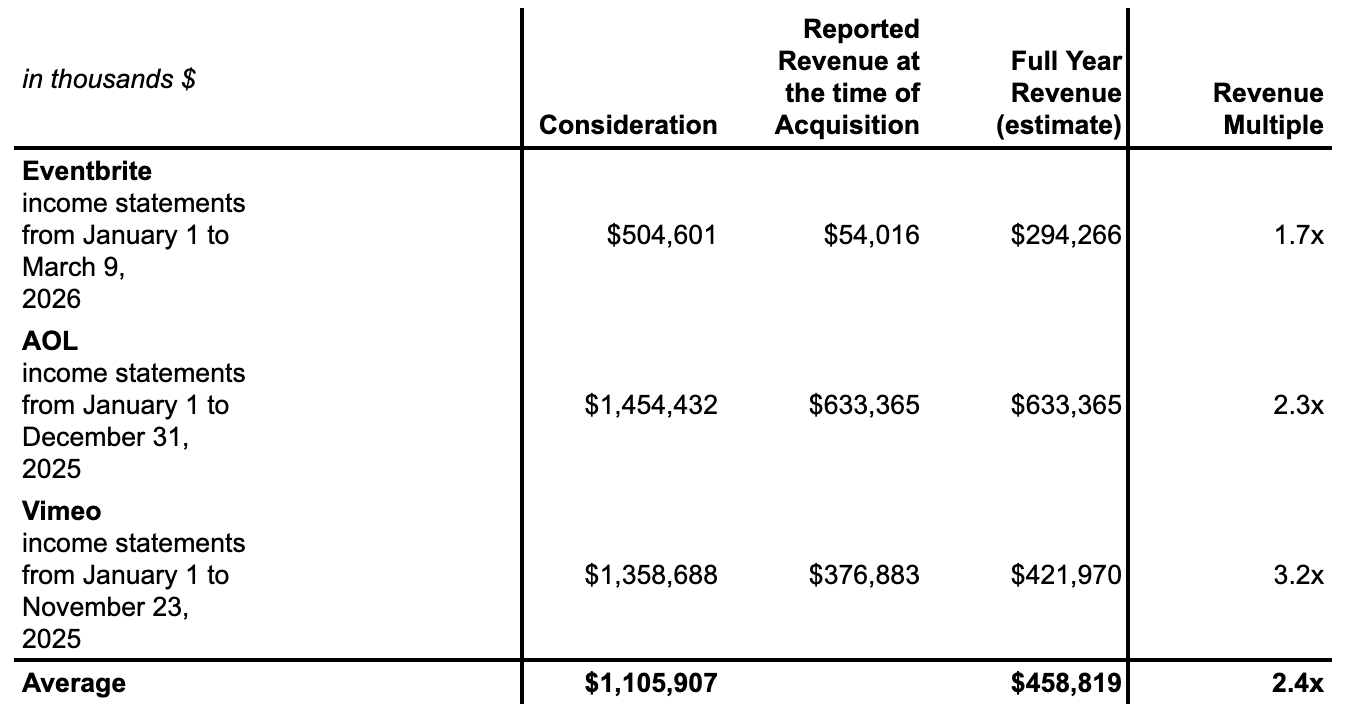

Bending Spoons' three larger acquisitions reported in its F1 filing are Eventbrite, AOL, and Vimeo, illustrating a disciplined approach to buying scaled digital assets at modest valuations.

Across the three transactions, the company deployed approximately $3.3 billion of capital to acquire businesses generating an estimated $1.37 billion in total annual revenue, equating to an average acquisition multiple of just 2.4x revenue. Eventbrite was acquired at only 1.7x revenue, AOL at 2.3x, and Vimeo at 3.2x.

These are not venture-style growth multiples, but rather value-oriented prices paid for established, cash-generating digital platforms that Bending Spoons believes can be materially improved through its operating playbook.

We think the consistency of these transactions is noteworthy. Despite differences in size and business model, Bending Spoons paid between 1.7x and 3.2x revenue for each of its three largest acquisitions. Combined with the company's 25% unlevered and 65% levered IRR hurdles, these valuations suggest a highly disciplined capital allocation framework. Rather than paying premium prices for growth, Bending Spoons appears to target mature software and internet businesses where operational improvements, rather than multiple expansions, are expected to drive the majority of shareholder returns.

Return Profile: One of the most striking aspects of the IPO filing is that Bending Spoons doesn’t evaluate acquisitions as a typical strategic buyer would. Every acquisition must clear a 25% unlevered IRR hurdle and an extraordinary 65% levered IRR hurdle, implying the company is only willing to pursue transactions where it believes its operational playbook can create exceptional value. For comparison's sake, a private equity firm looking to acquire, fix, and flip would typically expect…

One of the most striking aspects of the IPO filing is that Bending Spoons doesn’t evaluate acquisitions as a typical strategic buyer would. Every acquisition must clear a 25% unlevered IRR hurdle and an extraordinary 65% levered IRR hurdle, implying the company is only willing to pursue transactions where it believes its operational playbook can create exceptional value.

For comparison, a traditional private equity firm pursuing a buy-improve-sell strategy might underwrite a deal to generate an unlevered IRR in the low-to-mid teens and a levered IRR of roughly 20–25%. Bending Spoons' hurdle rates are materially higher on both measures, reflecting an exceptionally demanding investment discipline.

Rubber Meets the Road: Historical Financial Performance

Revenue: As of FY25, total revenue was $1.3 billion, including $603 million in 1Q26, with 84% from subscriptions, 12% from advertising, and 4% from other sources. We’ll come back to Bending Spoons’ advertising potential below.

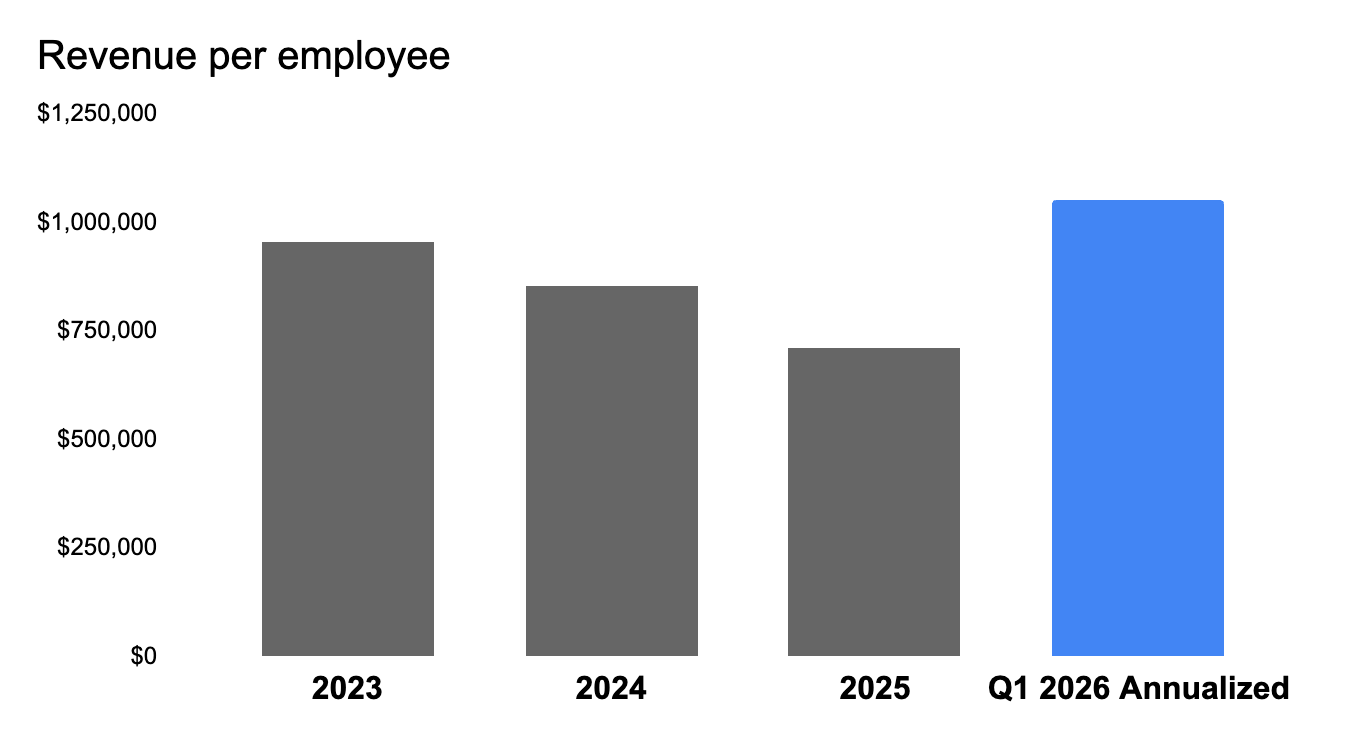

Revenue Productivity: Full-time equivalent team members, including both employees and contractors, totaled 405 at the end of 2023, 785 at the end of 2024, 1,834 at the end of 2025, and 2,284 at the end of Q1 2026. On an FY25 basis, revenue per employee was $712K. If we annualize 1Q26 revenue, Bending Spoons would generate over $1 million per employee.

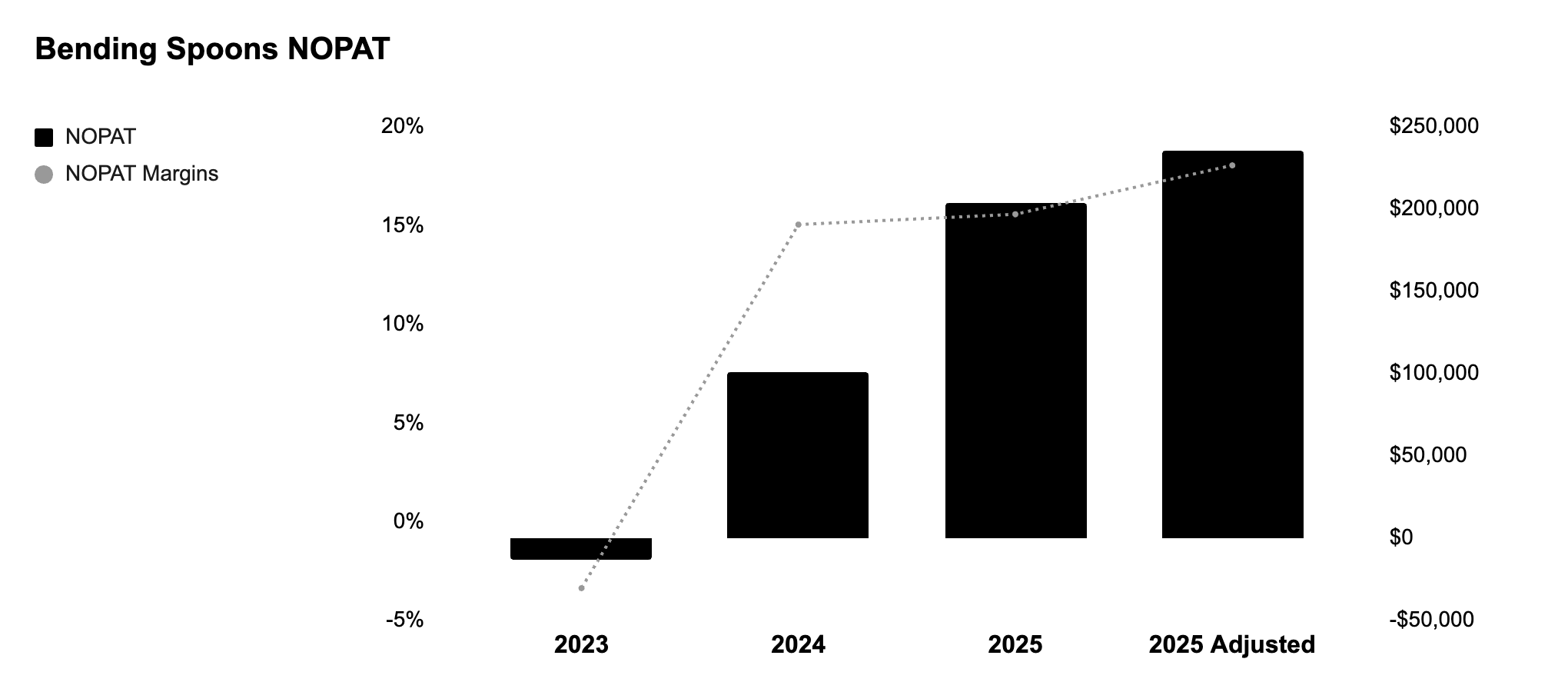

Operating profit (EBIT) was $278 million in FY25, generating a healthy EBIT margin of 21%. Management consistently delivered ~20% EBIT margins in 2023 and 2024 (a very good sign). After capitalizing 100% of R&D expenses over a 3-year period, as we prefer to do for tech companies, we arrive at an adjusted EBIT margin of 24% in FY25.

Net Operating Profit after Adjusted Taxes (NOPAT): After adjusting the tax effects of interest expense on debt and embedded capitalized lease interest to obtain a pure view of equity-holder flows, as well as changes in deferred taxes, Bending Spoons delivered $235 million in NOPAT and 18% margins. As a point of “gold standard” comparison, Google delivered an average NOPAT margin of 26% from 2019 to 2025 (with little variation), and Meta delivered an average margin of 36% over the same period.

Operating Invested Capital: In FY25, Bending Spoons’ operating invested capital (excl. non-operating items such as excess cash and goodwill) was $1.6 billion after adjusting for capitalized R&D treatment, generating a return on invested capital (ROIC) of 15%. We’ll come back to this all-important value driver later.

Investment Rate: As per management’s investment thesis, they are true to their word. In FY24 and FY25, the company invested 300% and 450% of NOPAT back into the business. We expect to see the same investment levels continue over the coming years.

Cost of Capital: Assuming a beta of 1.3 for our MarTech8 tracking portfolio and a 27% cash tax rate, we estimate a 10.5% cost of capital for Bending Spoons, resulting in a ~5% ROIC spread. Since management is aiming high, we again point to Google and Meta as the gold standard across all companies, which consistently generate 30%+ economic spreads (aka, pure free cash flow to equity holders).

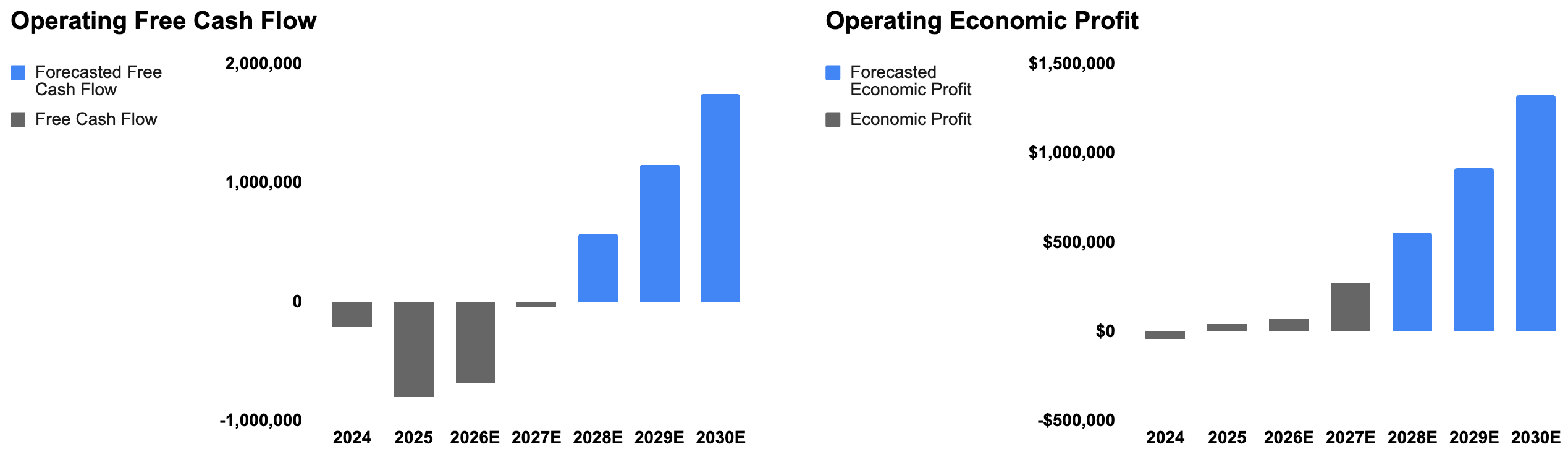

Operating Free Cash Flow: As our readers know, we focus only on pure free cash flow to equity holders, defined as NOPAT less changes in operating invested capital. For Bending Spoons, the company has not yet delivered positive free cash flow, but given the $21 billion post-IPO market cap, investors clearly believe the future is bright, and so does Quo Vadis.

Why is their belief already coming true? Because the difference between free cash flow (NOPAT minus net investment) and economic profit (economic spread over the cost of capital times invested capital) is exactly what we’d expect to see for a business model like Bending Spoons.

Where free cash flow asks:

“How much cash is left after funding future growth?”

Economic profit asks:

“Is management creating value on the capital already invested?”

Economic profit doesn’t care how much management is reinvesting. It only asks whether each dollar invested earns more than the cost of capital.

Bending Spoons is not attempting to maximize near-term free cash flow. Instead, management is deliberately reinvesting nearly all internally generated capital, and substantial external capital from its IPO, into acquisitions expected to earn returns well above the company's cost of capital.

As a result, free cash flow remains depressed during the investment phase even as economic profit is positive. This divergence is characteristic of successful capital compounders where value is created first through high-return reinvestment, while free cash flow emerges later as those investments mature. At least that is what Bending Spoons’ investors hope to see happen. We think it will.

Forecasting the Future

Returning to our key question:

What needs to be true in the future for the current market cap to hold?

Given the $21 billion post-IPO market cap, here’s what we think investors could theoretically be expecting from management over the coming years as a forecasting exercise:

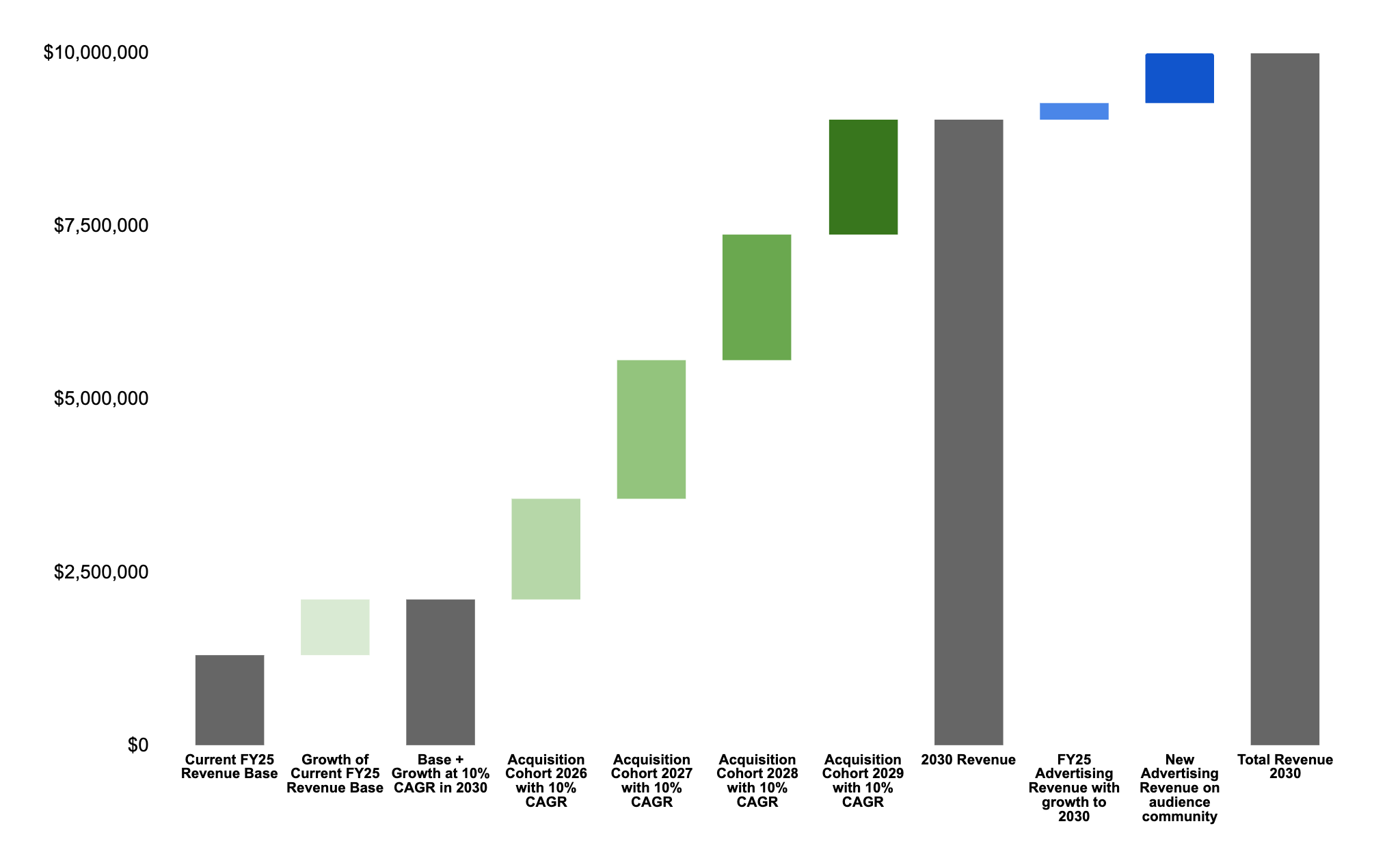

Total Revenue in 2030: From what we can observe, it seems reasonable to read through investor expectations and assume they expect around $10 billion in revenue by 2030. We can imagine growth coming from three areas:

Growth on the current revenue base starting with FY25

New Acquisitions of targets that meet the criteria mentioned above.

Advertising revenue growth by adopting a strategy similar to Amazon's and other retail media networks, where the lion’s share of ad revenue drops straight down to boost operating profits.

Growing Current Revenue Base: Let’s start our analysis by growing the current FY25 revenue base of $1.3B at a ~10% CAGR over the next five years, reaching $2.1B in 2030, with $7.9B in future revenue from new acquisitions and advertising.

New Acquisitions: Looking at a sample of the three acquisitions noted in Bending Spoons’ F1 filing (Eventbrite, AOL, and Vimeo), the average consideration was $1.4 billion, and the average acquired revenue was roughly $460 million on a ~2.4x revenue multiple.

Assuming the average future target generates $500 million in revenue, with acquisitions staggered throughout the year, we estimated management will need to identify and close two to three acquisitions per year through 2030 (not easy) and then grow revenue of each target at a 10% CAGR toward the $10 billion total revenue goal.

There are only ~5 months left in 2026, so we’d expect to see at least one to two more acquisition announcements this year. We then model out three acquisitions per year over the next three years: one in the first quarter, one at the halfway mark, and one in the latter half of each year through 2029. After assuming 10% annual revenue growth post-integration, we estimate ~$6.9 billion could materialize in 2030 from these new acquisitions.

The Third Growth Engine: Advertising

After modeling organic growth and future acquisitions, our forecast reaches approximately $9.25 billion in revenue by 2030, leaving roughly $750 million in additional revenue needed to support our $10 billion framework.

At first glance, this appears to be an aggressive assumption. But we think it is actually one of the more interesting opportunities embedded within the Bending Spoons story. Today, advertising represents just 12% of revenue, or approximately $156 million in FY25. Assuming this legacy advertising business simply grows alongside the existing portfolio, we estimate it will reach roughly $250 million by 2030, leaving approximately $750 million in incremental advertising revenue still to be generated.

As of the first quarter of 2026, management reported 500 million monthly active users across a portfolio that includes Vimeo, Eventbrite, WeTransfer, Meetup, Evernote, Brightcove, StreamYard, Remini, Splice and dozens of other consumer applications. Unlike a traditional software company, Bending Spoons increasingly owns hundreds of millions of daily consumer interactions.

Using conservative engagement assumptions, this audience could support hundreds of billions of annual advertising impressions. Under a more moderate scenario, the portfolio could generate more than one trillion annual advertising impressions. At industry net CPMs of roughly $2-$3, the theoretical revenue opportunity comfortably exceeds the $750 million required in our model, and that’s even before considering continued user growth with new acquisitions.

Importantly, we are not suggesting Bending Spoons should litter premium subscription products with banner advertisements. The larger opportunity likely lies in rewarded advertising, sponsored recommendations, commerce placements, creator monetization, native formats, and AI-personalized advertising experiences that complement rather than diminish the user experience.

The Amazon comparison is instructive. Amazon spent decades building one of the world’s largest consumer ecosystems before recognizing that every shopping session represented valuable commercial intent. Advertising became an incremental monetization layer built on top of an already profitable operating platform. Because the underlying customer acquisition, infrastructure, and software investments had already been made, much of each incremental advertising dollar flowed directly to operating profit. The same thinking applies to Bending Spoons to capture a new profit center.

Bending Spoons may now be approaching a similar inflection point. As management continues to acquire consumer applications, monthly active users should grow alongside revenue. If our revenue forecast proves directionally correct, the company’s audience in 2030 could be substantially larger than today’s 500 million monthly active users, creating an even larger advertising inventory than exists today.

From our vantage point, we think advertising has the potential to become not only a meaningful contributor to revenue growth but also one of the highest-return uses of the company’s existing consumer ecosystem.

A Logical Next Acquisition: AdTech

If advertising becomes Bending Spoons’ third growth engine, one strategic question naturally follows:

Why build an advertising platform when one can be acquired?

Rather than developing advertising technology organically, Bending Spoons could acquire an established ad technology company possessing the engineering talent, infrastructure, and commercial relationships required to monetize its growing portfolio of consumer applications. The ideal target would already specialize in areas such as rewarded advertising, web-app monetization, identity, creative optimization, and/or performance advertising.

Such an acquisition would simultaneously serve three strategic objectives:

First, it would immediately provide the technology stack necessary to monetize the hundreds of billions (and eventually trillions) of advertising impressions embedded across the existing portfolio.

Second, the acquisition would need to satisfy Bending Spoons’ exceptionally disciplined investment framework on its own merits. For example, a profitable ad technology company generating $100 million in gross ad spend, $30 million in revenue, and $10 million of EBITDA could continue operating as a standalone business while producing sufficient free cash flow to repay the acquisition investment within roughly three to five years.

In effect, Bending Spoons would be acquiring an advertising operating system while allowing the acquired company’s own cash generation to fund much of the purchase price. The advertising infrastructure required to monetize its internal inventory would therefore be obtained at little incremental economic cost.

Finally, the acquisition could establish Bending Spoons’ beachhead into an entirely new vertical. The advertising technology industry is currently in one of its most active consolidation periods in years. Independent ad networks, managed-service businesses, identity providers, creative technology companies, measurement platforms and other infrastructure providers are all facing mounting pressure from AI, privacy changes and increasing platform concentration. And several potential targets are profitable, founder-led or VC-friendly businesses trading at valuations well below historical levels.

As Warren Buffet says, “Be fearful when others are greedy, and greedy when others are fearful.” The Oracle from Omaha also advices, “Only when the tide goes out do you discover who's been swimming naked.”

For a company whose competitive advantage lies in operational excellence rather than product innovation, the ad environment appears remarkably familiar. Just as Bending Spoons has spent the last decade consolidating software businesses, the next decade could see it applying the same acquisition playbook to the advertising technology space by building not only one of the world’s largest collections of consumer software assets, but also the infrastructure that monetizes them.

Valuation Stack

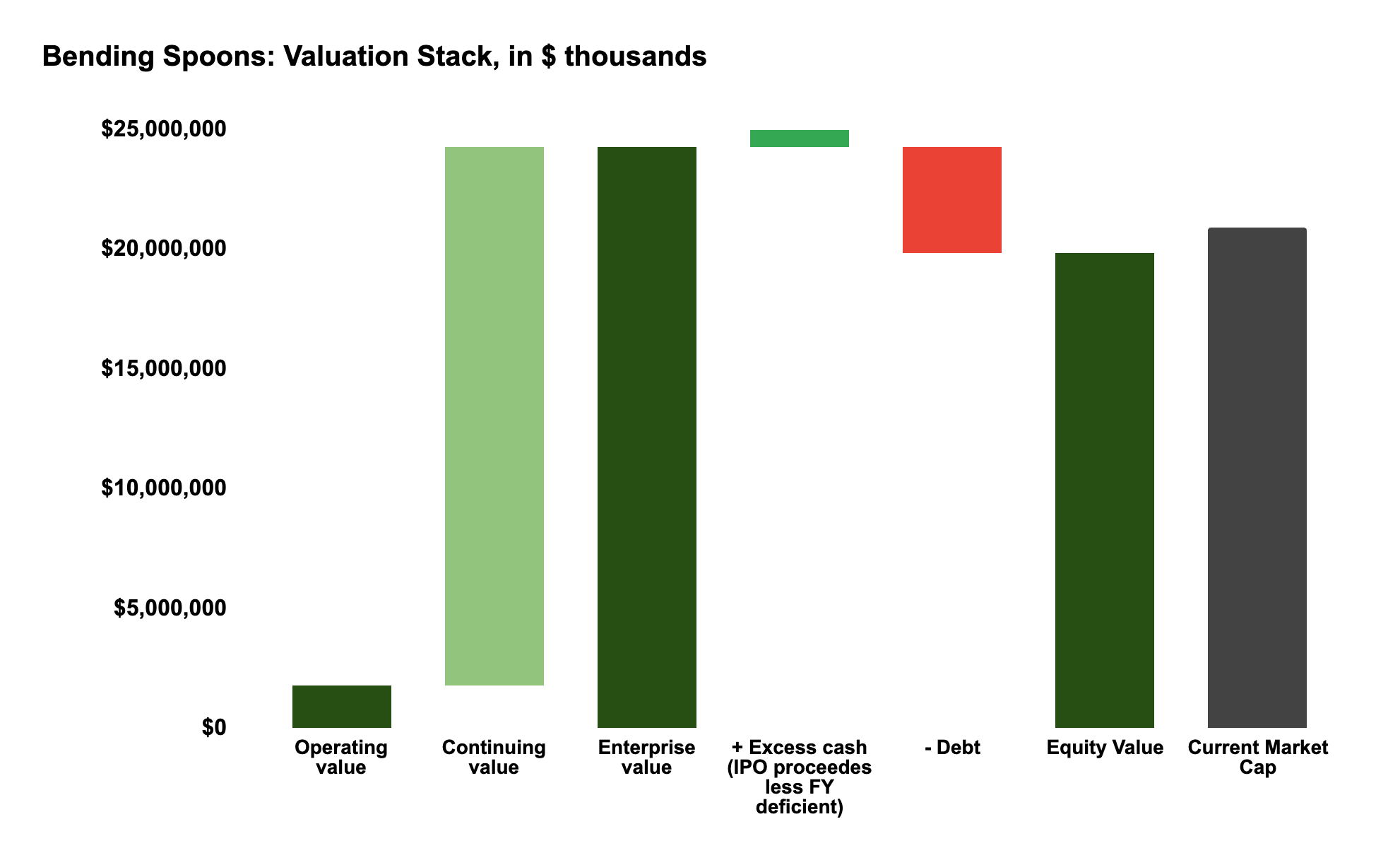

Our valuation framework assumes Bending Spoons expands its EBIT margin from 21% in 2025 to 30% by 2030, driven by scale and continued operating discipline. We model the cost of revenue declining from 34% to 30% of revenue and fixed operating expenses falling from 44% to 40% of revenue, reflecting management’s demonstrated ability to simplify operations, automate workflows, and leverage AI across an expanding portfolio.

Combined with improved capital efficiency from 0.76x to 1.66x in invested capital turns, our conservative assumptions drive ROIC from 15% today to 40% by 2030, placing Bending Spoons among the world's elite compounders.

Under these assumptions, the business would generate approximately $2.4 billion of NOPAT in 2030. Discounting those future cash flows yields an enterprise value of $24.2 billion and an equity value of $20.5 billion. The company's current market capitalization is also ~$20.5 billion.

Put differently, today's valuation already implies investors expect Bending Spoons to execute exceptionally well over the next five years, delivering both significant revenue growth and meaningful improvements in profitability and capital efficiency. We like what we see and wish them un sacco di buona fortuna!

Disclaimer: This post and any other post from Quo Vadis should not be considered investment advice. This content is for informational purposes only. You should not construe this information, or any other material from Quo Vadis, as investment, financial, or any other form of advice.