#151: 1Q26 Portfolio Update — AdTech, MarTech, BigTech and Agencies

Cannes Lions, Employee Productivity, LiftOff, Publicis/LiveRamp

#CannesLions is around the corner! Looking forward to seeing you at these events.

Commerce Media: See this series of Fluent events. Sir Martin Sorrell and I will have a chat and open it up to Q&A.

Agency Agentic Flows: 50-person RSVP breakfast with AtomicAds, the winner of the AdEF founder pitch event in March

Signal owners, platform leaders, and operators are rebuilding the layer underneath advertising. 50-person RSVP breakfast with Brian O’Kelley and Gabriel DeWitt, hosted by Above Data.

Criteo Lunch Panel: Measurement Models and Redefining Efficiency with Brian Wieser, Todd Parsons, and Tom Triscari

Buyer/Seller Agents: 25-person RSVP lunch with pubX

PMG Beach: How to Survive in a Post-LiveRamp World at PMG Beach: Sam Bloom, Mathieu Roche from ID5, and yours truly tell it like it is.

Criteo Yacht Talk: Wired Different. B.R.O.s at Work

C Wire AdTech Chill House: 1-1 chat with Sir Martin + Audience Q&A. We’ll end the week talking about what happened and why it matters.

1Q26 Portfolio Update

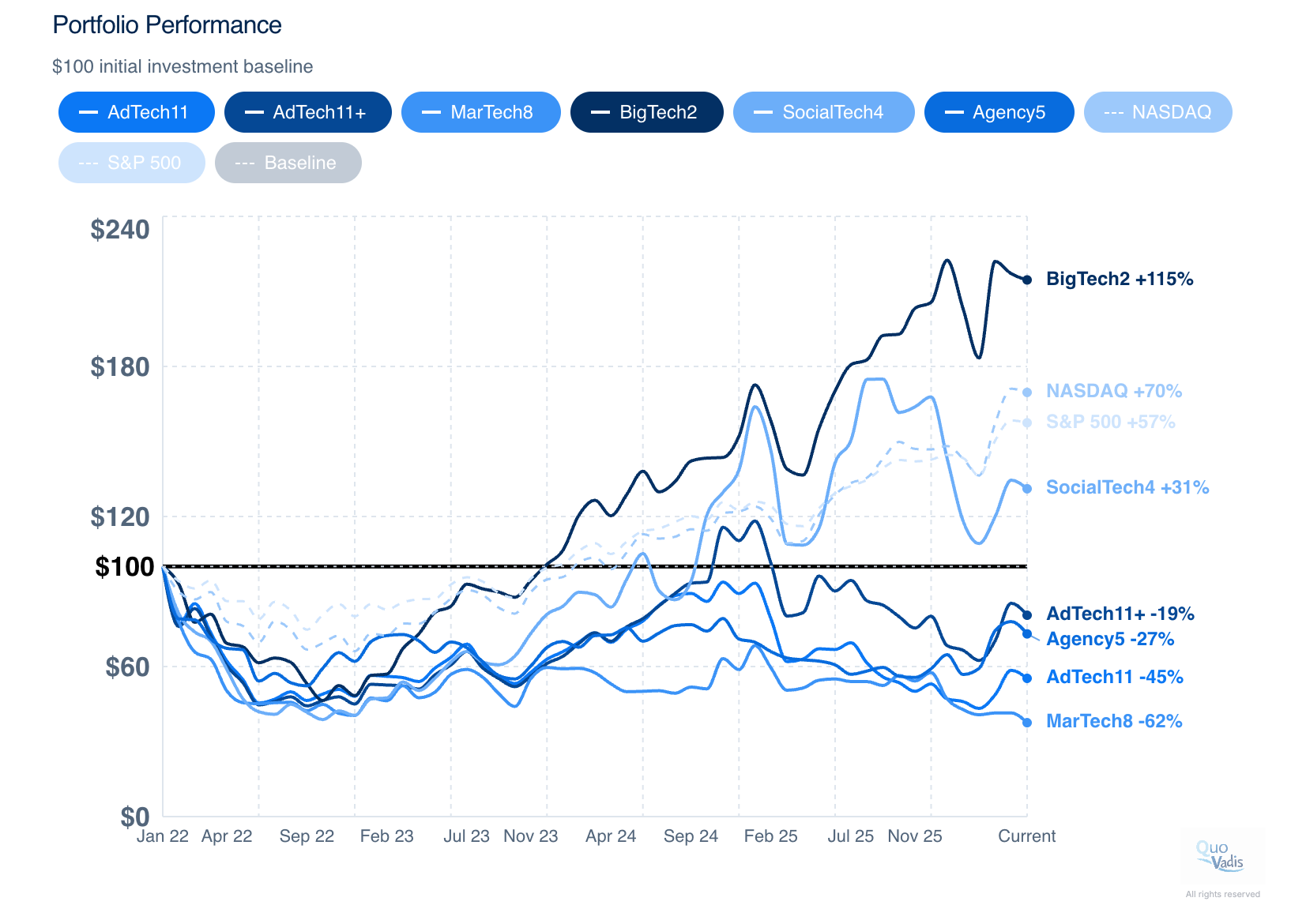

With 1Q 2026 earnings now reported, we can assess how our equal-dollar portfolios have performed since our 4Q25/FY25 update in early March.

As a reminder, each portfolio starts with a $100 investment in January 2022 divided equally across all constituent stocks. We rebalance on an equal-dollar basis whenever a constituent exits public life (IAS, RAMP, etc.) or when a relevant company goes public, like Mountain at this time last year and LiftOff today.

Liftoff’s (NASDAQ: LFTO) initial public offering began trading today. The company priced 19 million shares at $23 per share, which is above its marketed range of $20 to $22, raising ~$437 million in the offering.

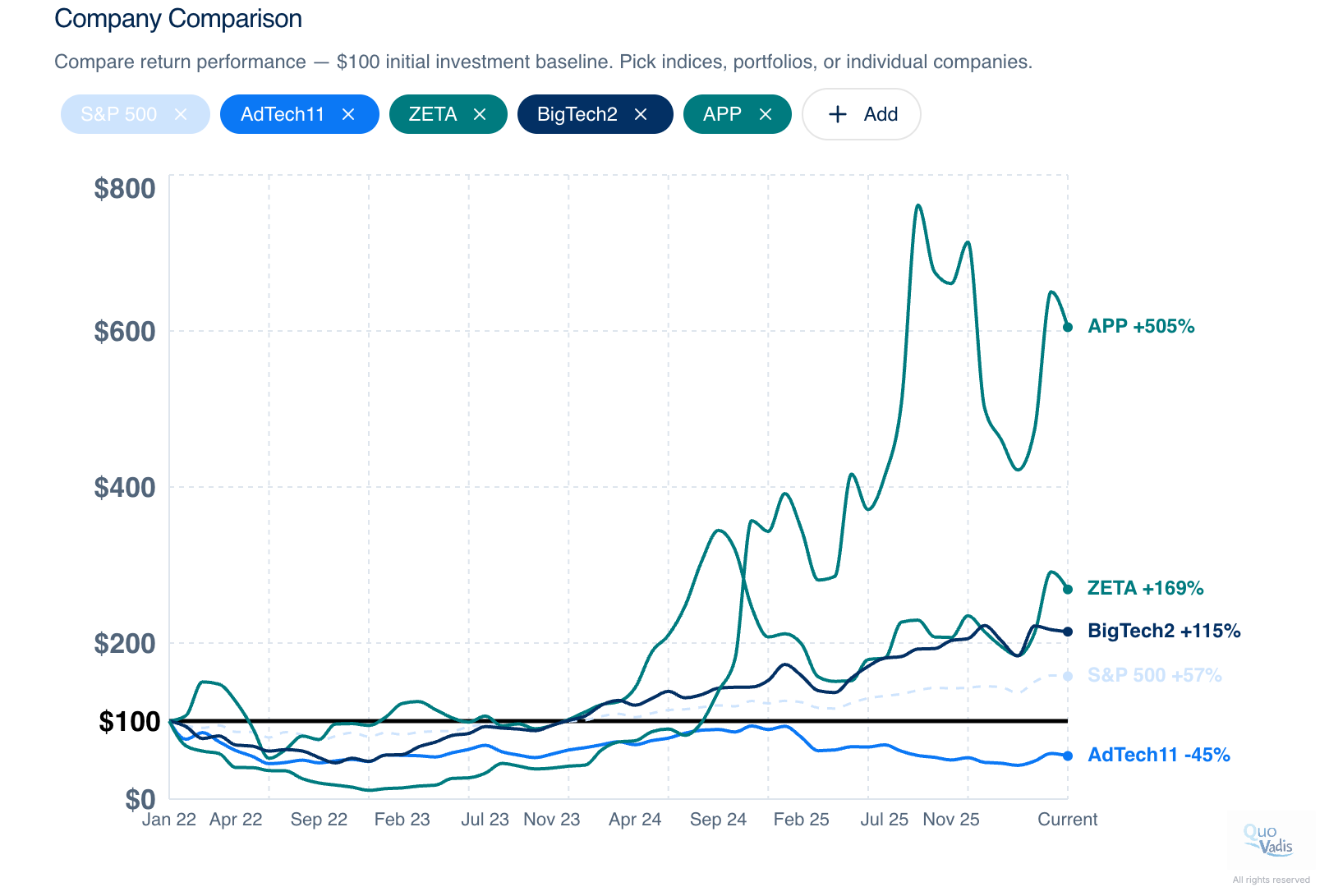

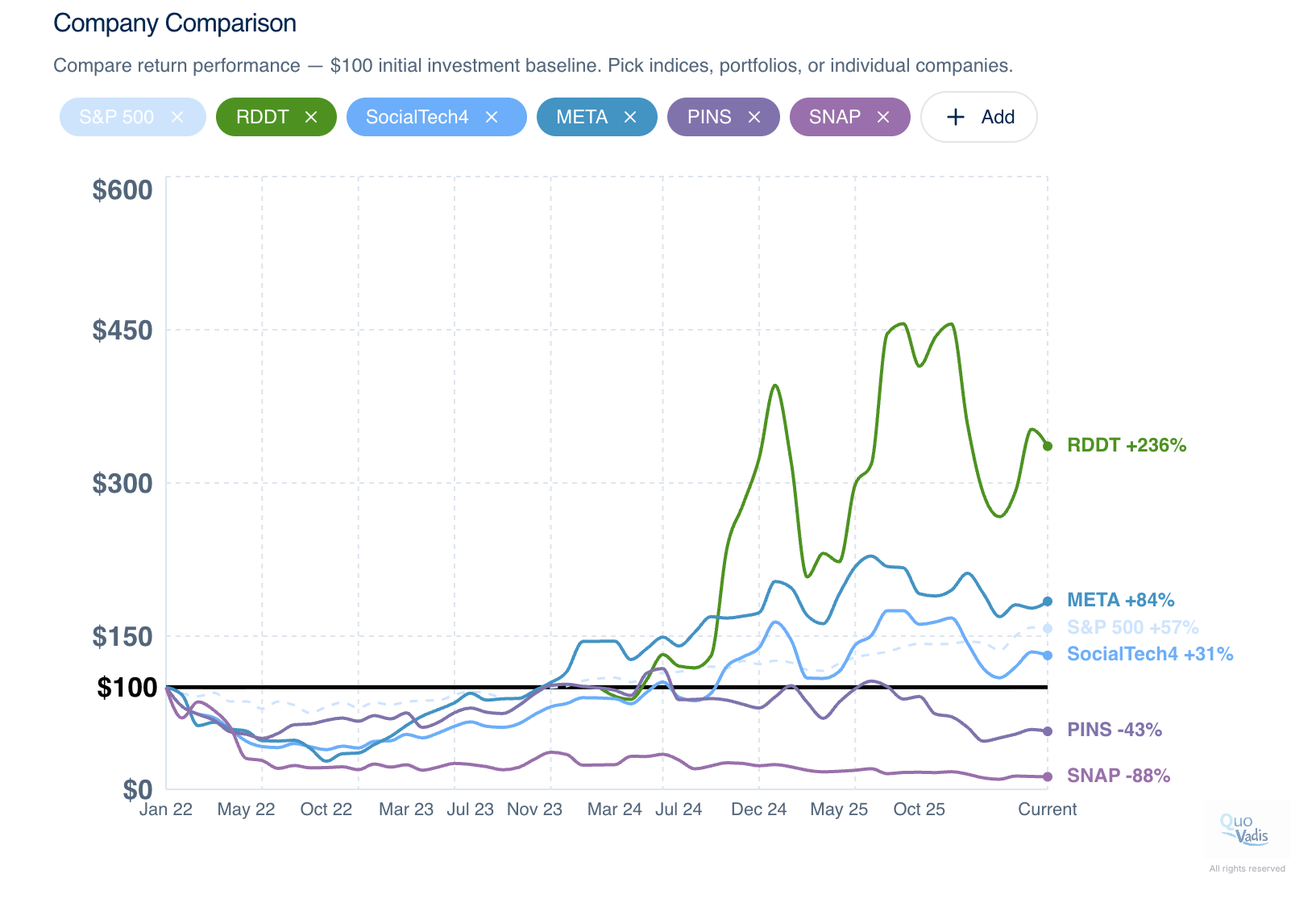

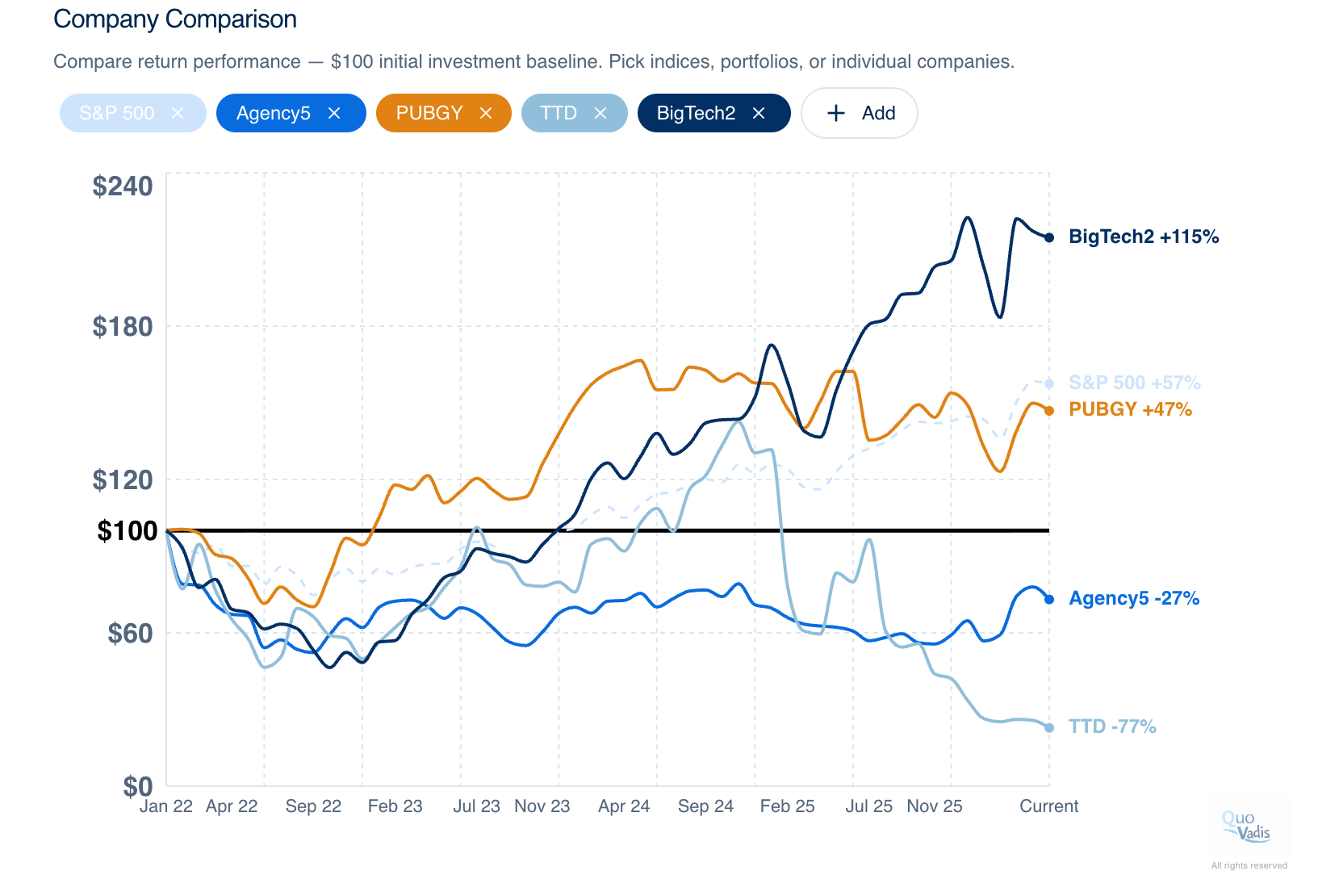

Benchmarks: Since January 2022, the NASDAQ and S&P 500 are up ↑70% and ↑57%, respectively.

BigTech2: We track two BigTech ad players, Google (GOOG) and Meta (META). Had you invested $100 on a 50/50 basis in January 2022, you’d be ↑115%. GOOG is up (+145%) and META (+84%) with nothing but blue sky ahead.

According to AdThena (search intelligence), Google is currently monetizing 0.1% of AI Overviews. What does that tell you?

These two companies are the “moat” gold standard of the advertising world. With ~45%+ return on invested capital, they are cash flow printing presses. Why? Because they own the best land (data) and farmers (advertisers) love renting it to get outcomes.

On a gross ad spend basis, Google Advertising delivers $2.1 million in revenue per employee, and Meta delivers $3 million. Notably, The Trade Desk tops both at $3.8 million per employee. If you’re a classic “AdTech” company in the private sector, we recommend finding a way to $1 million in revenue productivity as soon as you can. It drives all value creation.

AdTech11: Our AdTech11 portfolio is down ↓45% since inception. The portfolio includes: TTD, CRTO, DSP, ZETA, MGNI, PUBM, DV, TBLA, TEAD, RAMP, MNTN.

Zeta in the Spotlight: Zeta is the far-and-away top performer across the AdTech11, up ↑169%.

Looking at our AdTech11+ portfolio, which includes the flywheel known as Applovin, that company is up ↑5x since January 2022. If you’re interested in a great story from a top manager, check out this interview with Applovin CEO, Adam Foroughi.

Does Adam know what to do? Yes!

Does Adam get others (customers, employees, suppliers, investors, etc.) to do what he knows? Yes!

MarTech8: Our MarTech8 portfolio remains deeply in the red, down ↓62%. The portfolio includes: SHOP, HUBS, SPT, SEMR, TWLO, BRZE, YEXT, AMPL. This sector is clearly suffering from investor concerns about the creative disruption AI poses to the SaaS space.

SocialTech4: Our SocialTech4 portfolio is ↑31%. The portfolio includes: META, SNAP, PINS, RDDT. Reddit (RDDT) was added in April 2024 following its IPO and is up ↑236%.

Agency5: Our agency portfolio is down ↓27% since inception, and consists of Publicis (PUBGY), WPP, Omnicom (OMC), Stagwell (STGW), and S4 Capital (SCPPF). IPG was removed following its acquisition by Omnicom, which closed in late 2025.

From our perspective, it’s hard to ignore the dichotomy between Publicis’s top performance and The Trade Desk. From our perspective, the profile of Publicis’s M&A strategy over the past ~5 years reflects what we wrote in our piece called The Two Landowners of Adwell Hollow. When Arthur Sadoun took over in 2017, he decided it was better to be a landowner than a farmer, and that’s always a good bet.

With Google and Meta having amassed so much Sun Tzu power over the past two decades (~45% of all ad spend), Publicis decided to get in the game and play for keeps. And it’s working… very, very well!

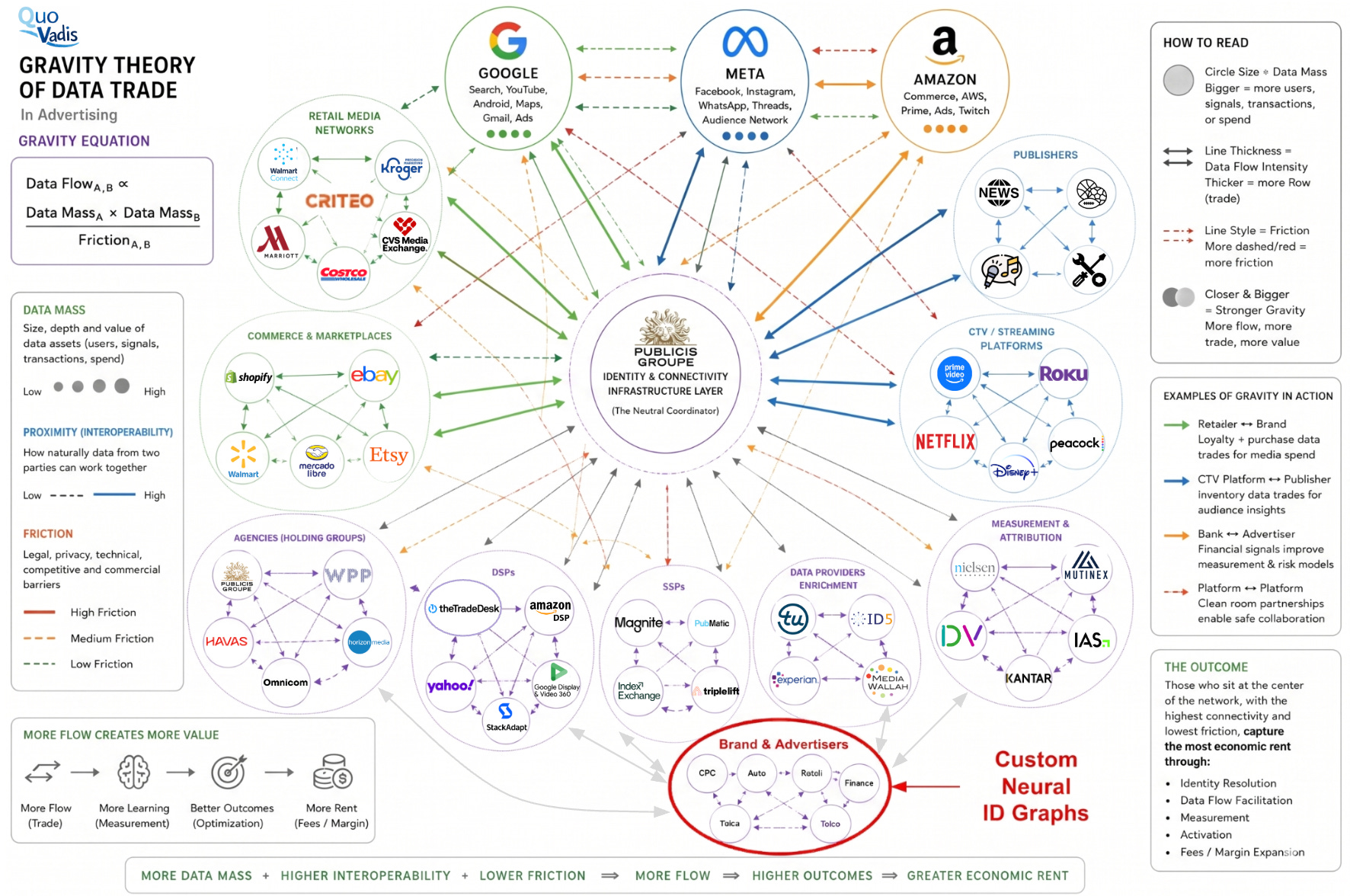

To that point, last we posted a piece called Publicis bought LiveRamp for a seat at the Identity Trade-Off Frontier and illustrated our view with a chart called The Gravity Theory of Data Trade. From Publicis’s perspective, the future of advertising is about owning the identity and connectivity layer that enables trusted data trade across brands, publishers, platforms, retailers, and media owners.

If we’re correct, Publicis wants to sit at the center of data gravity flows, capturing economic rent through identity resolution, measurement, activation, and collaboration. Time will tell.

Disclaimer: This post, and any other post from Quo Vadis, should not be considered investment advice. This content is for informational purposes only. You should not construe this information, or any other material from Quo Vadis, as investment, financial, or any other form of advice.